Top Finofo Alternatives for Canadians: 2025 Comparison Guide

Explore the best Finofo alternatives for Canadians. Compare features, compliance, and costs to find the ideal banking and AP automation solution for your business.

Trusted by 5,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

With Finofo changing which industries that they can serve in Canada, many Canadian businesses are looking for alternatives for their accounts payable automation and global payment solutions.

We reviewed all the payment solutions in Canada and created this guide to examine the top Finofo alternatives specifically for Canadian businesses. We'll compare platforms based on real local account infrastructure, CDIC protection, Canadian compliance requirements, and seamless accounting integration. Each alternative is evaluated through the lens of what Canadian businesses actually need: the ability to pay taxes and payroll, accept Interac e-Transfer®, maintain competitive FX rates, and integrate with QuickBooks or Xero.

Top Finofo Alternatives for Canadian Businesses in 2025

We evaluated each alternative based on Canadian compliance requirements, multi-currency support capabilities, AP automation features, and total cost transparency. Here are the platforms that best serve Canadian businesses seeking Finofo alternatives.

1. Venn – All-in-One Financial Platform for Canadian Businesses

Best for: Canadian SMBs needing comprehensive financial operations (AP automation, multi-currency accounts, corporate cards, expense management)

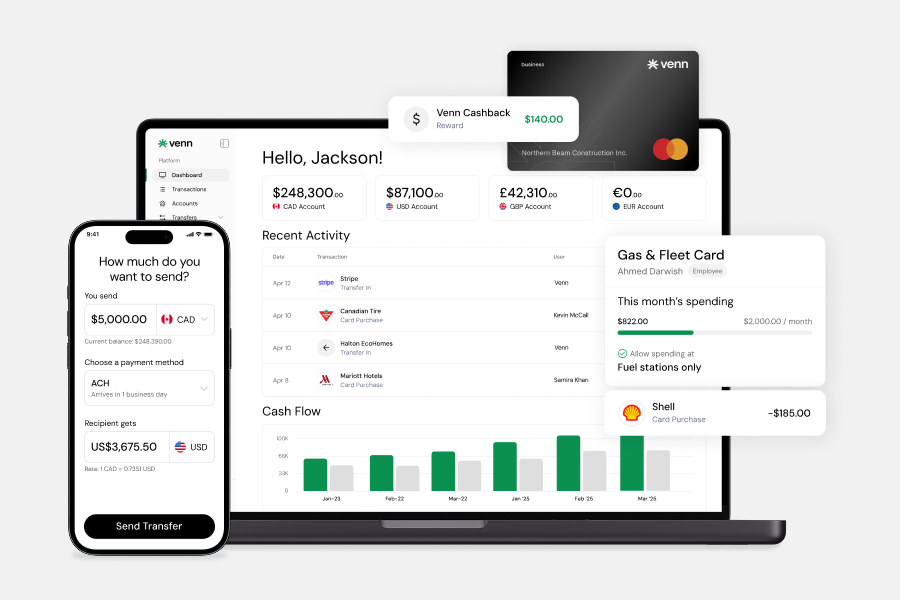

Venn stands apart as a complete financial platform that combines real local CAD, USD, GBP, and EUR accounts with AP automation, corporate cards, and deep accounting integration. Unlike platforms offering only virtual accounts, Venn provides actual Canadian and US account infrastructure through tier 1 banking partners.

This real account infrastructure makes Venn the only fintech platform where Canadian businesses can pay taxes directly, run payroll, and accept pre-authorized debits. The platform's comprehensive approach eliminates the need for multiple financial tools, consolidating everything from invoicing to expense management in one system.

Key features:

• Real local CAD and USD accounts with CDIC protection

• 1% unlimited cashback on all corporate card spend

• 2% unlimited interest on all USD/CAD balances

• FX rates from 0.25%, lowest in Canada

• Free unlimited Interac e-Transfer® on all plans

• Two-way sync with QuickBooks and Xero

• Built-in invoicing and expense management

• ACH, EFT, SEPA, UK Faster Payments support

• $6-10 global wires, free inbound wires

• Pay Canadian taxes, bills, and payroll directly

Venn's pricing structure stands out for its transparency and scalability. The Essentials plan includes no monthly account fees, with pricing based per account rather than per user. This means growing teams don't face escalating costs as they add employees. All plans include transparent FX rates with no hidden markups.

2. Wise Business – Multi-Currency Specialist

Best for: Businesses focused primarily on international transfers with minimal need for Canadian-specific banking features

Wise Business excels at international money transfers with transparent pricing and real exchange rates. The platform allows businesses to hold over 40 currencies and provides local account details in major currencies like USD, GBP, EUR, and AUD.

However, Wise's limitations become apparent for Canadian businesses needing comprehensive banking features. The platform doesn't support Interac e-Transfer®, lacks corporate card programs, and provides only basic integration with Canadian accounting systems.

Key features:

• Hold 40+ currencies

• Real exchange rate with transparent fees

• Local account details in USD, GBP, EUR, AUD

• QuickBooks and Xero integration

• No Interac e-Transfer® support

• No corporate card cashback program

• Limited Canadian banking integration

Pricing follows a pay-as-you-go model with fees typically ranging from 0.4% to 0.6% for currency conversion.

3. Corpay (formerly Cambridge Global Payments) – Enterprise FX Focus

Best for: Large enterprises with high-volume international payment needs and dedicated FX risk management

Corpay brings enterprise-grade foreign exchange services to the Canadian market, processing over $20 billion in B2B cross-border payments annually. The platform specializes in FX risk management with forward contracts and hedging tools that help large businesses manage currency exposure.

The enterprise focus means Corpay typically requires high minimum volumes and complex onboarding processes. Small and medium businesses often find the platform overwhelming and expensive compared to more accessible alternatives.

Key features:

• Enterprise-grade FX services

• Forward contracts and hedging tools

• Dedicated account management

• High minimum volumes typically required

• Limited AP automation features

• No corporate card program

• Complex pricing structure

4. BILL (formerly Bill.com) – AP Automation Focused

Best for: US-based companies with Canadian operations needing primarily AP workflow automation

BILL delivers robust accounts payable automation with sophisticated approval workflows and vendor management tools. The platform integrates well with accounting software and handles payment approvals efficiently.

Unfortunately, BILL's US-centric design creates friction for Canadian businesses. The platform charges additional fees for Canadian currency conversion and withdrawals, with international payment fees ranging from 1% to 3%. Without real Canadian account infrastructure or Interac e-Transfer® support, Canadian companies find themselves working around the platform's limitations.

Key features:

• Robust approval workflows

• Vendor management tools

• QuickBooks and Xero integration

• Limited multi-currency support

• No real Canadian account infrastructure

• Higher per-transaction fees for international payments

• US-focused feature set

5. Airwallex – Global Payment Infrastructure

Best for: High-growth tech companies with significant international payment volumes

Airwallex provides global payment infrastructure with an API-first approach that appeals to technology companies. The platform offers multi-currency accounts in over 11 currencies and competitive FX rates for high-volume transactions.

The technical complexity and lack of Canadian-specific features make Airwallex less suitable for typical Canadian SMBs. Without Interac e-Transfer® support or local Canadian banking features, businesses need additional platforms for domestic operations.

Key features:

• Multi-currency accounts in 11+ currencies

• Competitive FX rates

• API for payment automation

• Global collection accounts

• Limited Canadian-specific features

• No Interac e-Transfer® support

• Complex setup for non-technical users

Comparing Key Features Across Finofo Alternatives

Understanding how each platform addresses Canadian business needs helps narrow down the best choice. This comparison focuses on the features that matter most for companies operating in Canada.

How to Choose the Right Finofo Alternative for Your Business

Start by assessing your primary needs. If you mainly process international payments with minimal Canadian transactions, a specialized platform like Wise might suffice. However, most Canadian businesses need comprehensive solutions that handle both domestic and international operations equally well. Consider whether you need AP automation, corporate cards, expense management, or just basic payment processing.

Canadian-specific requirements often determine the best choice. Can you pay Canadian taxes and run payroll through the platform? Does it support Interac e-Transfer® for vendor payments? Are your funds protected under CDIC insurance? These aren't optional features for businesses operating primarily in Canada—they're essential for daily operations.

Evaluate the total cost of ownership beyond advertised monthly fees. Hidden FX markups can add thousands in annual costs. Per-user pricing models penalize growing teams. Transaction fees for common operations like EFTs or Interac e-Transfer® quickly accumulate. The most cost-effective solution often combines transparent FX rates, per-account pricing, and included transaction volumes.

Critical decision factors:

• Real local account infrastructure vs virtual accounts

• Canadian compliance and CDIC protection

• FX rate transparency and total markup

• Accounting software integration depth

• Corporate card benefits and expense management

• Pricing model (per user vs per account)

• Implementation complexity and migration support

Why Venn Is the Best Finofo Alternative for Canadian Businesses

Venn's comprehensive approach solves the fragmentation problem that plagues Canadian businesses using multiple financial platforms. Instead of juggling separate tools for banking, payments, cards, and expense management, Venn consolidates everything into one unified platform. This integration eliminates data silos, reduces reconciliation work, and provides complete visibility into company finances.

The real Canadian infrastructure advantage sets Venn apart from every competitor. Through partnerships with tier 1 Canadian banks, Venn provides actual local accounts that support pre-authorized debits, tax payments, and payroll processing. This isn't just convenient—it's transformative for businesses that previously needed traditional bank accounts alongside their fintech solutions. The CDIC protection on deposits provides peace of mind that funds are safeguarded.

Cost efficiency comes from both transparent pricing and platform consolidation. With FX rates starting at just 0.25%, Venn offers the lowest currency conversion costs in Canada. The 1% unlimited cashback on all corporate card spending effectively reduces operating expenses. Free unlimited Interac e-Transfer® and no per-user fees mean predictable, manageable costs as businesses grow.

Key differentiators:

• Only platform with real local CAD, USD, GBP, and EUR accounts

• Lowest FX rates in Canada (0.25% - 0.45%)*

• Free unlimited Interac e-Transfer® (only Canadian fintech offering this)

• 1% unlimited cashback with no minimum spend requirements

• Multi-currency card that automatically uses correct currency

• Pay Canadian taxes, bills, and payroll directly

• Two-way accounting automation with QuickBooks/Xero

• Pricing per account, not per user

• CDIC protection and RPAA compliance

Making the Switch: Migration Considerations

Finofo’s closure and industry payment restrictions created immediate risk for Canadian businesses running payroll, bill pay, and scheduled vendor transfers. The companies most affected operate in sectors like construction, trucking, real estate operations, trade services, and multi-currency SMB environments—industries that rely heavily on automated payments, bulk vendor transfers, and non-personal-guarantee corporate banking workflows.

Migration success starts with a workflow audit, not account setup. Begin by pulling a list of:

- active pre-authorized debit (PAD) pulls (e.g., payroll providers like ADP, Wagepoint, QuickBooks Payroll, or union insurance payments),

- scheduled bill pay automations (software tools, rent, telecom, fuel, equipment leases),

- recurring vendor transfers, and

- accounting or payroll software syncs.

From Finofo, export vendor profiles, PAD rules, and recurring payment schedules. If a platform can no longer pay certain sectors, flag those payments as highest-priority for cutover—especially anything tied to payroll or business-critical suppliers.

Short parallel runs protect vendor relationships. For payments that must not fail (payroll, logistics, or materials), update vendor PAD/bill credentials in your new platform and run both systems in parallel for 1–2 cycles. This validates that payroll pulls, PAD authorization, and supplier payments continue smoothly without chasing errors after the fact.

Conclusion

The landscape of Finofo alternatives offers various solutions, but Canadian businesses need platforms built specifically for their requirements. Real local account infrastructure, CDIC protection, Interac e-Transfer® support, and seamless Canadian compliance aren't optional features—they're fundamental to efficient business operations in Canada.

Venn stands alone as the only comprehensive platform combining real Canadian infrastructure with the lowest costs and full feature integration. By consolidating banking, payments, cards, and expense management into one platform with transparent pricing, Venn eliminates the complexity and hidden costs that force businesses to seek Finofo alternatives. Ready to experience banking built for Canadian businesses? Explore how Venn can transform your financial operations today.

Frequently Asked Questions

What is Finofo and why do businesses look for alternatives?

A: Finofo is an AP automation and multi-currency payment platform. Canadian businesses seek alternatives due to limited local banking integration, lack of Interac e-Transfer® support, missing CDIC protection, and inability to handle Canadian-specific needs like tax payments and payroll.

Can I use Venn to pay Canadian taxes and run payroll?

A: Yes, Venn's real Canadian account infrastructure supports pre-authorized debits, allowing you to pay taxes directly to the CRA and run payroll through Canadian payroll providers.

What makes Venn different from Wise or Airwallex?

A: Venn provides real local Canadian accounts with CDIC protection, free Interac e-Transfer®, corporate cards with 1% cashback, and the ability to pay Canadian taxes and payroll. Wise and Airwallex focus on international transfers without comprehensive Canadian banking features.

How does Venn's pricing compare to Finofo?

A: Venn offers transparent per-account pricing starting with no monthly fees on the Essentials plan, compared to Finofo's $$$29/month starting price. Venn includes free unlimited Interac e-Transfer® and the lowest FX rates in Canada (0.25%-0.45%).

Does Venn support Interac e-Transfer®?

A: Yes, Venn is the only Canadian fintech offering free unlimited Interac e-Transfer® on all plans, making it easy to pay Canadian vendors and contractors.

*Based on internal analysis comparing Venn's FX markup of 0.25%–0.45% to published rates from major Canadian financial institutions and fintech platforms as of November 2025.

---

**Disclaimer:** This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 5,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 5,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.