Venn vs. Plooto: Full Financial Operating System vs. Specialized Payments Platform

For Canadian companies managing complex payables, receivables, and team finances, two modern platforms stand out: Venn and Plooto. But their strengths and design philosophy are quite different.

Trusted by 10,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

For Canadian companies managing complex payables, receivables, and team finances, two modern platforms stand out: Venn and Plooto. But their strengths and design philosophy are quite different.

Plooto focuses specifically on automating accounts payable (AP) and accounts receivable (AR) workflows. It’s best known for digitizing cheque issuance, syncing bills and payments with QuickBooks or Xero, and streamlining how businesses get paid.

Venn, by contrast, is an all-in-one financial platform. It replaces traditional business banking for Canadian companies by offering multi-currency accounts (CAD, USD, GBP, EUR), corporate cards with cashback, AP/AR automation, global transfers, and even investment options all in one unified dashboard.

This guide breaks down the major differences between the two platforms feature by feature so you can choose the best solution for your company’s stage and scope.

Venn vs. Plooto: Feature Comparison at a Glance

Let’s compare Venn vs. Plooto at a glance. Here’s how the two solutions differ across their most important features:

Feature: Global accounts and business banking

Venn

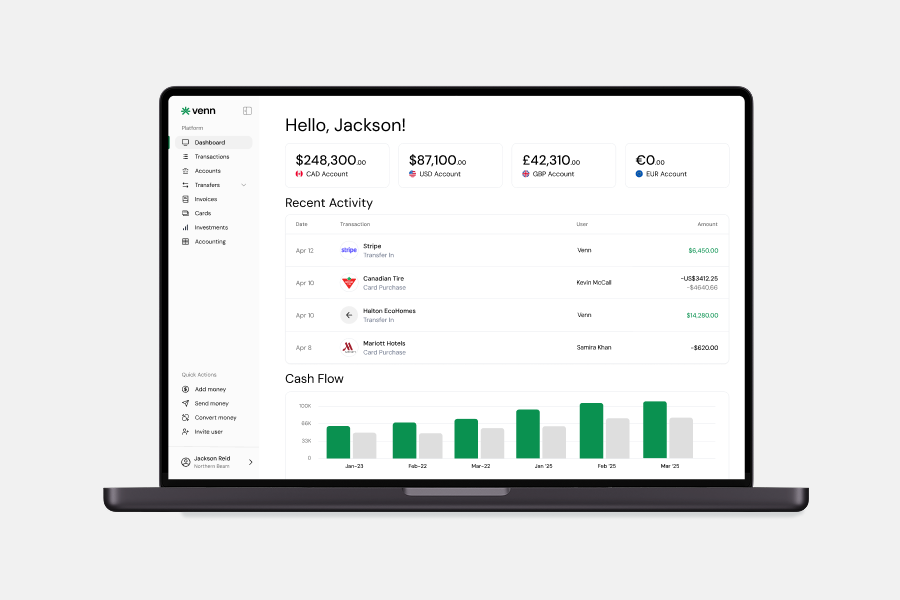

Venn offers fully integrated multi-currency accounts in CAD, USD, GBP, and EUR, making it a comprehensive financial platform for Canadian businesses operating across borders. These accounts are issued through regulated financial partners and designed to support real operational needs, whether it's holding balances, paying vendors, or receiving international transfers. Venn also offers interest on balances, paying 2% annually on all USD/CAD holds on the platform. This unlocks new revenue streams for your business without any additional steps or work.

Funds can be managed directly within the Venn platform, including sending Interac e-Transfers®, making domestic and international payments, and syncing seamlessly with your accounting tools. There are no monthly fees, and because these are actual local currency accounts, they help reduce FX conversion costs and avoid cross-border transaction fees common with traditional providers.

Plooto

Plooto is focused on streamlining payments and accounting, specifically accounts payable and receivable. While it facilitates CAD and USD transactions, it does not offer users access to integrated, in-platform multi-currency accounts. Instead, users connect their existing business bank accounts and cards to send or receive funds.

As a result, any actual currency holding, inbound transfers, or bank reconciliation is handled through an external institution. This keeps Plooto squarely in the AP/AR automation space rather than functioning as a financial hub for day-to-day operations. For users who need true multi-currency infrastructure and consolidated controls, this is where Venn delivers a deeper, all-in-one experience.

Feature: Global transfers and FX functionality

Venn

Venn provides a fully integrated approach to global transfers and foreign exchange. With native multi-currency accounts in CAD, USD, GBP, and EUR, businesses can hold balances and send payments in over 40 currencies to more than 200 countries.

Transfers can be initiated using EFT, ACH, SEPA, and UK Faster Payments, with funds typically arriving within the same business day or the next. These local transfers can also be sent for free in the Pro and Plus plans. This makes cross-border operations faster, more cost-effective, and fully transparent.

FX fees start as low as 0.25% on the Pro plan, and Venn’s pricing is clearly outlined by plan tier, helping businesses forecast international costs without surprise markups.

You can learn more about Venn’s global transfers here.

Plooto

Plooto supports international vendor payments to 40+ countries and enables businesses to send funds via EFT or ACH using their linked external business bank accounts. However, it does not offer built-in multi-currency accounts, so payments must be initiated from your own CAD or USD account (or a linked credit card), and FX conversions are handled at the point of transaction.

International payment delivery typically takes 5 to 7 business days unless you opt for Plooto Instant, which speeds up transfers but may come with added fees. The Go plan charges a flat $19 FX fee per international transfer, while the fee is waived on Grow and Pro plans.

Plooto's FX functionality is serviceable for basic AP/AR use cases but less suited for businesses that require multi-currency holdings or frequent global transfers.

Payments & FX (Table)

Feature: Accounts Payable for Managing Outgoing Payments

Venn

Venn provides a fully integrated Accounts Payable suite that supports a wide range of payment types including EFT, ACH, SEPA, UK Faster Payments, and Interac e-Transfers. Bills can be pulled directly from accounting software and categorized automatically, reducing manual effort. Venn also supports multi-step approval workflows with user roles and permissions, making it a good fit for finance teams that require more granular control over payments.

All local EFT and ACH payments are free on Venn’s Pro and Plus plans, and international wire fees are competitively priced depending on plan tier ($6 - $10 per wire). The AP module is natively part of Venn’s all-in-one platform, enabling real-time visibility and tighter control across all outgoing financial activity. This makes Venn an ideal solution for growing businesses that want to unify payments and approvals without relying on multiple external systems.

Plooto

Plooto is specifically designed around AP and AR workflows and is often used by accounting professionals managing client payables. It supports domestic payments via EFT and ACH, and also enables CRA tax payments and paper cheque issuance, which is something Venn does not offer.

However, users must link an external bank account or fund payments via a personal or business credit card. On the base Go plan, each EFT or ACH payment costs $1, though this drops to $0.50 on Grow and Pro tiers. Plooto’s strength lies in streamlining payment approvals and audit trails, with controls over who can authorize payments and modify rules. For firms that prioritize AP and tax payments over broader banking functionality, Plooto provides a targeted solution.

Feature: Invoicing / Accounts Receivable (AR)

Managing AR is essential to cash flow, and both Venn and Plooto offer invoicing features to help businesses get paid faster, though their focus differs.

Venn

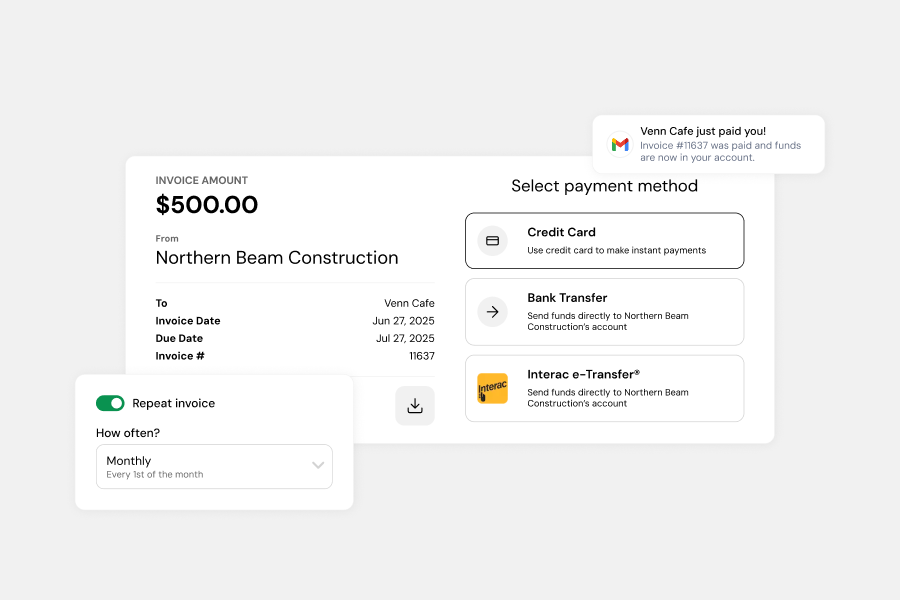

Venn’s invoicing product is tightly integrated with the rest of the platform, allowing users to issue branded, multi-currency invoices directly from their account. Businesses can accept credit card or bank transfer payments, and there are flexible options to determine who pays processing fees. Invoicing also connects with Venn’s AP and accounting features, creating a single source of truth for both receivables and payables.

Recurring invoicing, auto-categorization, and seamless reconciliation make Venn suitable for companies that want to eliminate friction from the AR process without using a separate invoicing tool. The integration with Venn’s native multi-currency accounts is especially valuable for businesses that invoice in CAD, USD, GBP, or EUR.

Plooto

Plooto includes basic invoicing tools that let users send payment requests via ACH or EFT. While it supports automated payment reminders and tracks invoice status, it lacks more advanced capabilities like recurring billing or custom invoice templates. Payments can be accepted via credit card, though a 2.9% fee applies.

Plooto is optimized for accountants or bookkeepers managing payables and receivables on behalf of multiple clients. Its AR functionality is more about facilitating incoming payments efficiently than building out a full invoice lifecycle experience. For businesses that need AR as part of a broader financial operating system, Venn provides more functionality out of the box.

Feature: Bank Reconciliation & Accounting Integrations

For finance teams, smooth integration with accounting systems is critical to minimize manual data entry and streamline reconciliation processes. Both Venn and Plooto integrate with major accounting tools, though the impact of those integrations varies based on how each platform operates.

Venn

Because Venn is a full-stack financial platform that includes banking, payments, AP/AR, and expense management, it provides a much more complete dataset to accounting software like QuickBooks and Xero. The platform offers true two-way sync, ensuring that transactions, receipts, and bills are all automatically categorized and matched. This helps reduce errors, save time, and increase visibility across the finance function.

By managing funds directly within Venn’s ecosystem, there’s no need to reconcile data from an external bank. Everything from expense receipts to vendor payments flows through the same ledger, which simplifies audit trails and accelerates month-end close.

Plooto

Plooto also integrates well with QuickBooks and Xero, and supports NetSuite on its higher-tier plans. Its syncing capabilities work well for businesses that use Plooto strictly for AP and AR, allowing for easier posting of payment transactions and tracking of outstanding bills. However, because Plooto does not include its own accounts or cards, reconciliation often involves cross-referencing data from the user’s bank, Plooto, and accounting software.

This makes it less streamlined compared to Venn, where financial activity is unified under one roof. Still, for accountants who already manage their clients’ bank accounts separately, Plooto’s focused integration can be a practical and familiar workflow.

Feature: Corporate cards for your team

Venn

Venn provides a unified corporate card solution directly tied to its integrated multi-currency accounts. Each card supports spending in CAD, USD, GBP, and EUR, enabling businesses to transact in local currencies without needing separate conversions or incurring additional FX fees.

Venn supports instant issuance of both physical and virtual cards at no extra cost. Businesses can set custom spend limits, apply real-time controls, and manage merchant-level permissions. All card transactions earn 1% cashback with no minimum spend requirement, making the cards not just convenient but also financially rewarding.

Plooto

Plooto does not issue corporate cards or virtual cards. Instead, it allows users to make payments using their connected business bank account or a personal or business credit card. If a credit card is used to fund an EFT or ACH transaction, a 2.9% fee applies.

This setup enables businesses to maintain flexibility in funding payments, but it lacks the built-in controls, real-time visibility, and cashback benefits that Venn’s native corporate card program offers. Since Plooto does not support card issuance, businesses looking to manage employee spend at scale or centralize financial controls across departments may need to rely on additional third-party tools.

Venn vs. Plooto: Pricing Overview

Venn and Plooto both offer tiered pricing structures, but their value propositions differ significantly based on the depth of functionality included in each plan.

Venn’s Pricing Structure

Venn offers three transparent pricing tiers that scale with your business needs. Each plan includes access to multi-currency accounts, corporate cards, and integrations—while reducing FX and wire fees as you upgrade.

Essentials (Free – $0/month)

- FX Fee: 0.45%

- Local Transfers (EFT/ACH): $2 each

- International Wires: $10

- Up to 20 virtual cards and 3 physical cards

- Multi-currency accounts (CAD, USD, GBP, EUR)

- Integration with QuickBooks and Xero

- Basic receipt automation

- 1% cashback on card spend, capped at CAD 5,000/month

- 2% interest on all CAD/USD balances

- Best For: Small businesses and startups that need essential financial tools and basic multi-currency support.

Plus ($40/month)

- FX Fee: 0.35%

- Local Transfers: Free

- International Wires: $8

- All Essentials features included

- 50 virtual cards and 10 physical cards

- Custom roles and access permissions

- 10 sub-accounts for departmental or project tracking

- Automated accounting rules

- Receipt capture and categorization

- 1% cashback on card spend, capped at CAD 25,000/month, no minimum spend required

- 2% interest on all CAD/USD balances

- Best For: Growing businesses that need enhanced card access, better expense management, and scalable financial controls.

Pro ($100/month)

- FX Fee: 0.25%

- Local Transfers: Free

- International Wires: $6

- All Plus features included

- Unlimited virtual and physical cards

- Unlimited sub-accounts

- Multi-step approval workflows

- Instant payment clearing

- Priority support

- Dedicated account manager

- Unlimited 1% cashback on all card spend

- 2% interest on all CAD/USD balances

- Best For: Larger businesses or enterprises handling international payments, multiple departments, or advanced financial workflows.

Plooto’s Pricing Structure

Plooto is structured around three tiers focused on AP/AR management. Pricing varies based on included controls and whether FX and transaction fees are waived.

Go ($9/month)

- EFT/ACH Fee: $1 per transaction

- International FX Fee: $19 per transfer

- Basic AP/AR functionality with payment scheduling

- QuickBooks and Xero integration

- Credit card payments accepted (2.9% fee applies)

- No access to corporate cards or multi-currency accounts

- Best For: Small firms managing occasional vendor payments or accountant-led setups needing light AP tools.

Grow ($32/month)

- EFT/ACH Fee: $0.50 per transaction

- International FX Fee: Waived

- All Go features included

- Enhanced controls for payment methods and approval rule changes

- Audit trail capabilities

- NetSuite integration available

- Best For: Mid-sized businesses needing more control over payment approval and a lower transaction cost structure.

Pro ($99/month)

- EFT/ACH Fee: $0.50 per transaction

- International FX Fee: Waived

- All Grow features included

- Extended compliance tools and advanced payment approval workflows

- Suited for multi-entity or more complex accounting setups

- Best For: Larger accounting firms or finance teams managing high volumes of AP/AR across multiple clients or departments.

Venn: Strengths & Considerations

Here's a look at the strengths and considerations of the Venn platform:

Pros:

- All-in-One Financial Platform: Venn consolidates business banking, accounts payable, accounts receivable, global transfers, corporate cards, and expense management in a single system.

- Integrated Multi-Currency Accounts: Businesses can manage balances in CAD, USD, GBP, and EUR natively, enabling both local and international operations without relying on external banks.

- Corporate Cards with Real-Time Controls: Instantly issue virtual and physical cards with customizable spending limits, role-based approvals, and real-time tracking. All card spend earns 1 percent cashback with no minimum.

- Built-In Expense Management: From receipt automation to accounting sync and approval routing, Venn enables full visibility into team expenses.

- Strong AP and AR Automation: Venn supports domestic and international vendor payments through EFT, ACH, SEPA, UK Faster Payments, and Interac e-Transfers. It also enables businesses to invoice and accept credit card payments directly.

- Two-Way Accounting Integrations: Deep integrations with QuickBooks and Xero make reconciliation smoother and reduce manual effort.

- Transparent Global Payments and FX Fees: FX rates are as low as 0.25 percent, with wire fees starting at six dollars. Transfers typically settle in zero to one business days.

- Unified Platform Experience: Because Venn offers both accounts and tools, there is no need to sync external banks. Everything is managed in-platform.

- Transparent, Flat Pricing: Monthly pricing tiers are simple and upfront. EFT and ACH are free on paid plans, with no surprise markup or usage caps.

- CDIC Insurance: Venn is a PSP in Canada, meaning that up to $100,000 of your funds are protected

Considerations:

- Newer in Market Compared to Legacy Tools: Venn is a fast-growing platform, but newer compared to long-standing accounting-led tools. While its functionality is expanding rapidly, some users may initially seek the familiarity of more narrowly scoped legacy platforms.

Plooto: Strengths & Considerations

Here is a breakdown of Plooto’s benefits and tradeoffs, particularly in the context of its specialization in accounts payable and receivable automation:

Pros:

- Focused AP and AR Automation: Plooto streamlines invoice and bill payments with features like payment scheduling, auto-reconciliation, and support for recurring payments.

- CRA Payment Support: Businesses can use Plooto to submit CRA tax remittances, which is valuable for compliance-driven workflows.

- NetSuite Support on Higher Tiers: In addition to QuickBooks and Xero, Plooto also integrates with NetSuite on premium plans, which may appeal to mid-market teams.

Approval Controls: Grow and Pro plans include permissioning for payment method and rule changes, improving audit readiness and team accountability. - Cheque Issuance: Unlike Venn, Plooto supports issuing paper cheques, useful in industries where certain vendors still require them.

Considerations:

- No Multi-Currency Accounts: Plooto does not provide its own accounts, meaning businesses must link external CAD or USD bank accounts to initiate payments.

- Limited to AP and AR Use Cases: Plooto is not an all-in-one platform and does not support corporate cards, employee spend tracking, or international expense management.

- Higher Transaction Costs on Lower Plans: On the Go plan, each EFT or ACH payment costs one dollar, and FX fees are a flat nineteen dollars per transfer. These costs can add up for high-volume businesses.

- Longer International Payment Times: Payments may take five to seven business days unless you pay extra for Plooto Instant. Funding still requires external bank accounts or credit cards.

- No Native Expense or Card Management: There are no features for managing team spend, issuing cards, or receiving cashback on purchases.

Which Platform Is Right for Your Business?

Choosing between Venn and Plooto depends on whether your business needs a complete financial platform or a dedicated accounts payable and receivable workflow tool.

Venn is ideal for businesses that want to manage their finances in one place. From paying vendors and collecting invoices to issuing cards, tracking expenses, and moving funds across borders, Venn offers the infrastructure to simplify financial operations. With multi-currency accounts, built-in automation, and transparent pricing, Venn reduces friction, cost, and reliance on external banks or bolt-on tools. It is a compelling fit for startups and scaling businesses seeking end-to-end visibility and control.

Plooto is best suited for accountants, bookkeepers, or finance teams that primarily need to automate payables and receivables. Its tools are focused but limited in scope. Businesses that already have established banking relationships and only need help managing payments and approvals may find Plooto a practical addition to their workflow.

For companies that want to centralize financial operations, reduce costs, and modernize their payment infrastructure, Venn stands out as the more complete and scalable solution.

Ready to Transform Your Business Finances with Venn?

Discover how Venn can simplify your business banking, streamline your spending, and empower your global operations.

Learn More About Venn's All-in-One Platform

Frequently Asked Questions (FAQs)

Q: Can Venn fully replace Plooto for AP/AR automation?

Yes. Venn includes integrated accounts payable and receivable functionality with the added benefit of native multi-currency accounts, corporate cards, and local (Interac e-Transfer®) and international payment capabilities. Plooto is more narrowly focused on structured AP/AR workflows and requires linking an external bank account, while Venn provides a broader, unified platform for end-to-end financial operations.

Q: Does Plooto offer multi-currency accounts or local balances like Venn?

No. Plooto requires users to connect their existing Canadian or U.S. bank accounts to fund payments and does not provide native multi-currency accounts (CAD, USD, GBP, or EUR). In contrast, Venn includes built-in multi-currency accounts on every plan, allowing businesses to hold foreign balances directly within the platform and avoid unnecessary FX costs.

Q: Are there differences in international payment speed between Venn and Plooto?

Yes, Venn is significantly faster. Venn enables international transfers to over 200 countries with settlement typically in 0 to 1 business day and transparent FX fees as low as 0.25 percent. Plooto supports fewer countries (40+) and standard payments can take five to seven business days (unless paying extra for "Plooto Instant").

Q: Which platform provides better visibility and control over team spending?

Venn offers full real-time spend management built-in, including unlimited virtual/physical corporate cards, role-based permissions, and transaction-level controls. Plooto is solely focused on vendor payments (AP/AR) and does not issue cards or track employee spend. For managing both vendor invoices and employee purchases in one system, Venn is the consolidated solution.

Q: How do the platforms handle accounting integrations?

Both Venn and Plooto integrate with major accounting tools like QuickBooks Online and Xero. Plooto also supports NetSuite on premium plans. However, Venn’s integrations go further by combining banking, card, and AP/AR data into a unified, two-way feed before syncing, simplifying reconciliation compared to Plooto, which must rely on separate bank data for complete transactional insight.

The comparative information provided on this page is based on publicly available sources and is accurate to the best of our knowledge as of July 30, 2025. Features, pricing, and terms may change without notice. For the latest information, please consult each provider’s official website directly. All trademarks and product names are the property of their respective owners. Their use does not imply any affiliation with or endorsement by those brands.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 10,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 10,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.