Profit First Method: A Practical Guide for Canadian Small Businesses

What is the Profit First method and how the Profit First accounting works at a high level, how to adapt it for Canadian-incorporated small businesses, and where a platform like Venn can make the operational side easier.

Ahmed Shafik

Co-founder

Trusted by 10,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

Profit is whatever is left after bills, payroll, and taxes. That’s how most businesses operate, but it’s also why so many struggle with cash flow when margins tighten or unexpected costs hit.

The Profit First® method flips that logic. Instead of treating profit as whatever remains at the end, you treat it as an upfront allocation. You set aside profit and tax first, then operate the business with what’s left.

What is the Profit First method?

The Profit First® method was created by Mike Michalowicz and introduced in his book Profit First. Profit First® is a registered trademark of Mike Michalowicz.

The traditional formula most business owners learn looks like this:

- Sales – Expenses = Profit

The Profit First method inverts it:

- Sales – Profit = Expenses

You choose your profit percentage ahead of time. Whenever revenue comes in, you move that portion (along with owner’s pay and tax) into separate buckets. The remaining balance becomes your true operating budget.

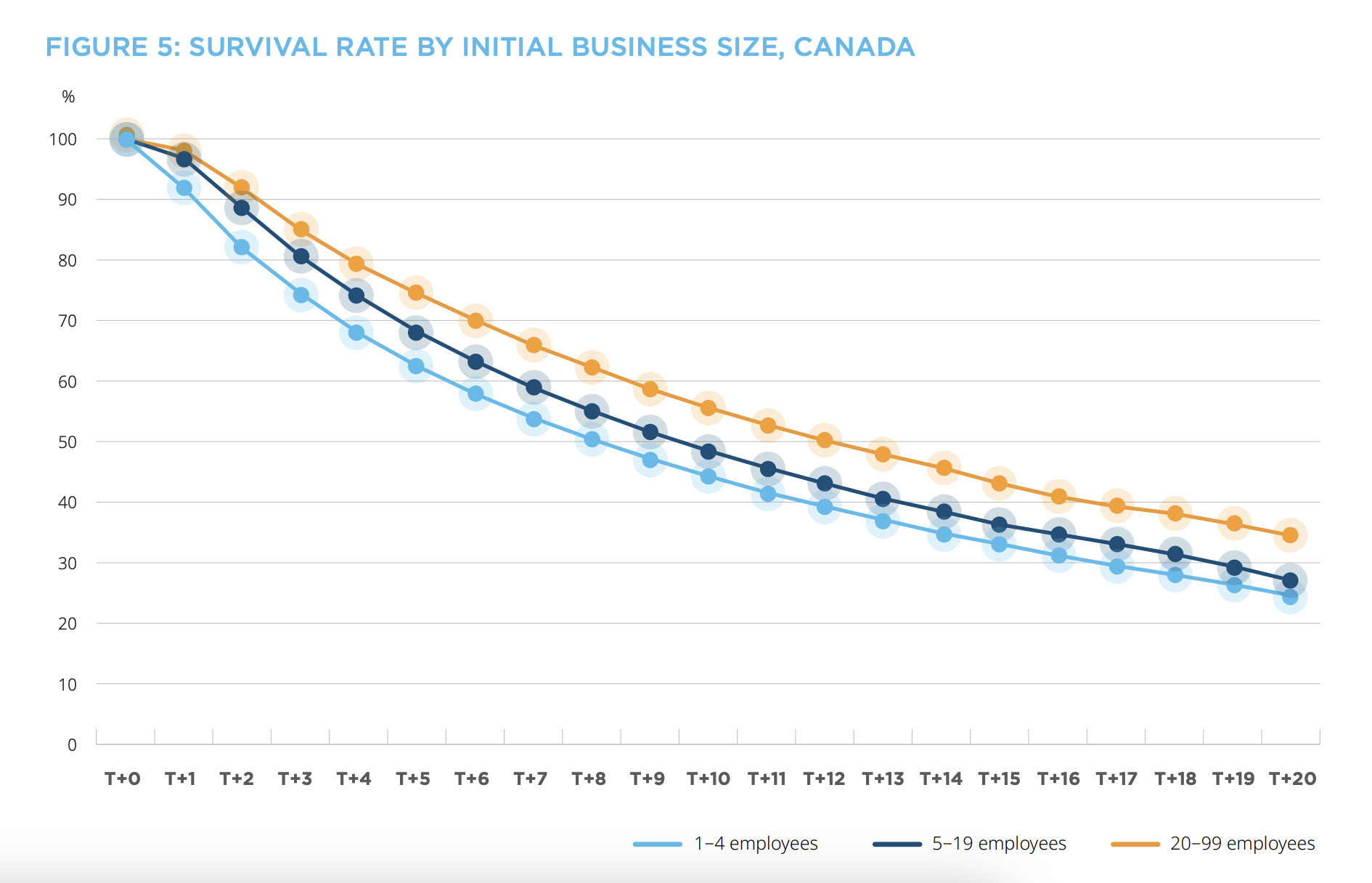

This matters because early-stage businesses are financially fragile. Federal data shows that only 62.5% of Canadian businesses with 1–4 employees survive five years. Treating profit as a non-negotiable line item helps owners avoid running the business on whatever happens to be left over.

It is important to note that Profit First accounting does not replace your official bookkeeping or tax filings. It is a cash management framework that sits on top of your existing accounting system:

- Your accountant still prepares financial statements and tax returns according to Canadian rules.

- Profit First influences how you move actual money between accounts.

- You still need to track GST/HST, payroll, and corporate tax in line with CRA requirements.

How Profit First fits Canadian businesses

The core concepts of Profit First for small business are global, but Canadian companies need to layer in local tax and regulatory realities, particularly GST/HST and corporate tax.

GST/HST and the small supplier threshold

In Canada, most businesses must register for GST/HST once their worldwide taxable supplies exceed $30,000 in a single calendar quarter or over four consecutive calendar quarters.

Once you are registered, the GST/HST you collect belongs to the government. Under a Profit First approach, it makes sense to move GST/HST into a dedicated tax bucket regularly so it is not accidentally used to fund everyday operating expenses.

Here's how to register for a GST/HST number in Canada.

Corporate tax and year-end pressure

For incorporated companies, corporate income tax is another predictable outflow. The timing may vary, but the obligation does not. Profit First encourages you to set aside a percentage of revenue into a tax bucket all year, instead of scrambling to cover a large balance after your accountant finalizes the return.

CRA guidance explains how businesses calculate and remit corporate tax based on their taxable income and filing frequency, but the exact rate varies across provinces and income levels.

The specific percentage should be set with your accountant, based on your historical effective rate and expected profitability.

A high-level overview of Profit First for small business

Here are the core steps behind the Profit First method so you can see how it works in practice.

Step 1: Map your cash flow and obligations

Before you change anything, you need a clear picture of:

- Average monthly revenue over the last 6–12 months

- Fixed costs like rent, software, and payroll

- Variable costs like contractors, marketing, or inventory

- GST/HST you collect and remit

- Corporate income tax pattern, if you have at least one filed year

This is also a good time to confirm whether you are correctly registered for GST/HST and charging the right rate.

Step 2: Create simple buckets for profit, pay, tax, and expenses

In the original Profit First framework, businesses use multiple accounts to simulate envelopes for different purposes. At a high level, you will usually see buckets for:

- Profit

- Owner’s compensation

- Taxes

- Operating expenses

Some owners also add buckets for things like debt repayment or major future investments. We outlined the specific account setup and naming in our Profit First Account setup guide.

For now, the important point is separation. Profit and tax money should not be sitting in the same pot you use for day-to-day bills.

Step 3: Choose starting percentages

Next, decide what share of each dollar of revenue will go toward the key buckets. There is no universal formula, but many Canadian service businesses start with modest targets such as:

- Profit: 1–5%

- Owner’s pay: a fixed percentage that covers your personal income needs

- Tax: a percentage based on prior-year effective tax rates and GST/HST

- Operating expenses: whatever is left

E.g. suppose your corporation brings in $60,000 in a month and your starting allocations are:

- 5% to Profit

- 15% to Tax (including GST/HST)

- 35% to Owner’s pay

- 45% to Operating expenses

You would move:

- $3,000 into Profit

- $9,000 into the Tax bucket

- $21,000 into Owner’s pay

- $27,000 remains available for operating costs

If those allocations feel impossible, Profit First has done its job. It is showing you that your current cost structure and pricing do not support the margin you want. You can then adjust pricing, reduce overhead, or modify allocations while you work toward healthier targets.

Step 4: Move money on a regular schedule

Instead of moving funds every time a customer pays an invoice, most businesses set fixed allocation days. A common pattern is twice per month.

On those days, you:

- Look at the balance of your main income account.

- Apply your percentages to calculate how much should be moved into each bucket.

- Transfer those amounts into the separate accounts for Profit, Owner’s pay, Tax, and Operating expenses.

The operating account is then used to pay vendors, subscriptions, and other day-to-day costs. If the operating bucket is empty, the answer is not to dip into tax or profit. The answer is to rework expenses or pricing.

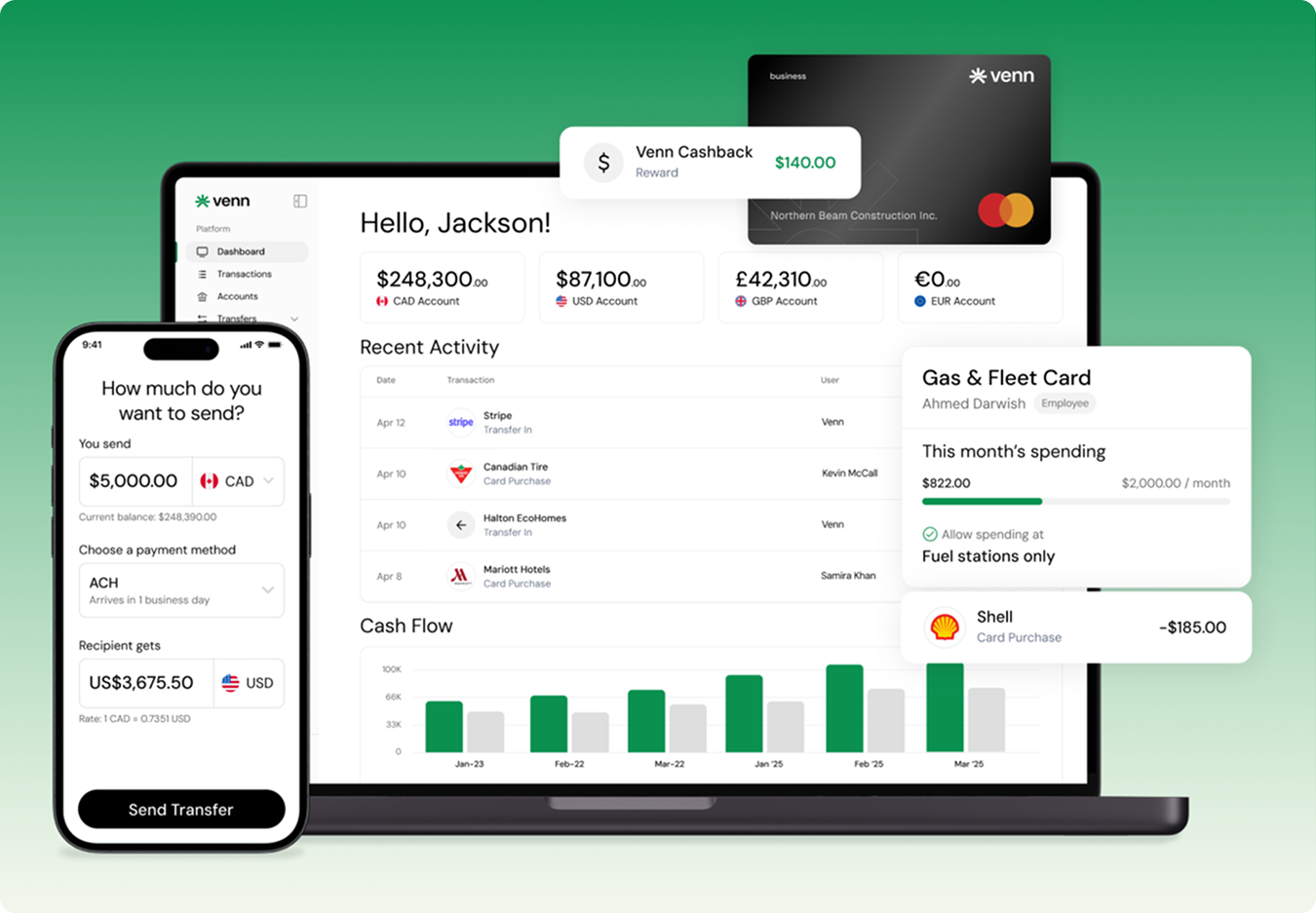

Venn’s tools can simplify this process:

- Issue invoices, receive payments in CAD or foreign currencies, and centralize receivables so your allocation days are based on up-to-date balances.

- Use Global Transfers to pay domestic and international vendors from the correct bucket, including cost-effective local and cross-border payments in a range of currencies.

Why the Profit First method works for Canadian SMBs

You do not need to adopt every element of the Profit First method to benefit from its core principles. Even partial implementation can improve decision-making for Canadian-incorporated businesses with 1 to 50 employees.

Profit becomes intentional instead of incidental

By treating profit as a planned allocation rather than a residual, you:

- Put a minimum profit level into your operating model.

- Force trade-offs between new spending and protected profit.

- Avoid relying solely on top-line growth to improve margins.

Independent explanations of Profit First consistently highlight this shift toward deliberate, habit-based profitability.

Tax bills become more predictable

Moving GST/HST and estimated corporate tax into a dedicated bucket as revenue comes in helps you:

- Avoid treating tax amounts as available for regular expenses.

- Reduce the risk of needing short-term financing or emergency cuts at filing time.

Funding tax provisions gradually is one of the safest ways to avoid cash flow strain when returns are due.

Cash flow decisions become clearer

With a defined operating expense bucket, it becomes easier to answer questions like:

- Can we afford another hire on our current revenue base?

- Does this new lease or software contract fit our budget?

- Do we need to raise prices before committing to a new expense?

Instead of guessing based on a single account balance, you make decisions from a clearer view of what is already reserved for profit, tax, and owner compensation.

Modern tools reduce friction

When Profit First was first introduced, many owners moved money manually. Today, platforms like Venn can reduce the operational effort:

- Global Accounts let you hold CAD, USD, GBP, and EUR balances with local account details, which helps you keep Profit First buckets in the currencies you actually use.

- Accounting Automation integrates with QuickBooks and Xero, helping you reconcile multi-account activity without duplicating work.

- Corporate cards linked to the platform give you granular spend controls, so your operating expense bucket is supported by real-time visibility and limits rather than after-the-fact review.

Where the Profit First method can be challenging

No single framework works for every business at every stage. The Profit First method is no exception.

High overhead or tight margins

If your current margins are very thin, even a small initial profit percentage may feel unrealistic. Starting with small percentages and adjusting gradually rather than forcing a target that your business cannot support yet is a better strategy.

In practice, that might look like:

• Starting with 1 or 2 percent profit.

• Using the structure to highlight where pricing or cost reductions are needed.

• Revisiting your allocations quarterly with your accountant.

Fast-growth, high-investment companies

Some high-growth startups intentionally reinvest most available cash into product, sales, or expansion. A strict Profit First allocation might feel misaligned with investor expectations during heavy investment phases.

Even so, these companies can still borrow elements of Profit First accounting, such as:

• Maintaining a dedicated tax bucket.

• Protecting a small profit allocation as a stability buffer.

• Using separate buckets for operating expenses and debt repayment.

Existing debt

If your corporation already carries significant debt, you may want an adapted version of the framework that includes a dedicated debt reduction bucket. Many advisors who use Profit First in practice suggest creating a specific allocation for debt alongside profit and operating expenses, rather than leaving it in the same pool as everything else.

In all of these scenarios, working with a Canadian accountant or Profit First–literate advisor is recommended to make sure your approach matches your sector, tax position, and risk tolerance.

Is the Profit First method right for your business?

The Profit First method is ultimately about priorities and discipline. Instead of hoping there is profit left at the end of the year, you design your operations so that profit, owner compensation, and taxes are funded from the start.

For Canadian-incorporated small and midsize businesses outside Quebec, adopting Profit First in full or in part can help you:

- Build profit into your operating model rather than treating it as an accident.

- Manage GST/HST and corporate tax provisions more predictably.

- Make clearer decisions about hiring, overhead, and expansion.

- Use modern tools like Venn to handle the practical side without adding manual work.

If you want to explore this further, practical next steps could include:

- Reviewing your last 6 to 12 months of cash flow with your accountant and agreeing on realistic starting percentages.

- Setting up simple buckets inside your existing financial platform for profit, owner’s pay, tax, and operating expenses.

- Reading our upcoming article dedicated to Profit First accounts, where we will break down account types, naming, and workflows in more detail.

Profit First works best when it’s paired with financial infrastructure that keeps profit, tax, and operating funds clearly separated. Venn makes that separation easy: dedicated CAD and foreign-currency accounts, smart controls on spend, and fast payment rails that keep cash flow predictable.

If you want a Profit First system that’s actually workable inside a busy Canadian business, Venn gives you the foundation to do it.

Frequently Asked Questions (FAQ)

Q: Is Profit First an accounting system?

A: No, Profit First is a cash-flow management framework. You still need traditional bookkeeping and tax filing under Canadian standards, and you should rely on your accountant for compliance. Profit First® simply changes how you organize and allocate cash inside your operating accounts.

Q: Do I need special software to run Profit First?

A: Not necessarily. Many Canadian businesses run it using basic accounts and scheduled transfers. However, tools that offer multiple accounts, controlled spending, and clean payment workflows—like Venn—make it easier to maintain the structure without adding admin work.

Q: Can I use Profit First if my revenue fluctuates seasonally?

A: Yes. Profit First is especially helpful for seasonal businesses. Allocating profit, tax, and owner’s pay as a percentage of every inflow helps smooth cash year-round instead of depending heavily on peak-season months.

Q: Does Profit First work for businesses with payroll?

A: Yes. Many companies add a dedicated payroll bucket so payroll always has priority funding. This helps ensure payroll stays protected from unexpected expenses. This structure is explained fully in our Profit First accounts guide.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Profit First® is a registered trademark of Mike Michalowicz, who created the method and detailed it in his book Profit First. Venn is not affiliated with or endorsed by Mike Michalowicz or the Profit First brand; this article is an independent guide to applying the method.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 10,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 10,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.