Virtual Cards: 10 Real Advantages & Drawbacks for Canadian Businesses

Discover the top 10 pros and cons of virtual cards for Canadian businesses. Learn how to streamline spend and avoid common pitfalls with the right provider.

Trusted by 5,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

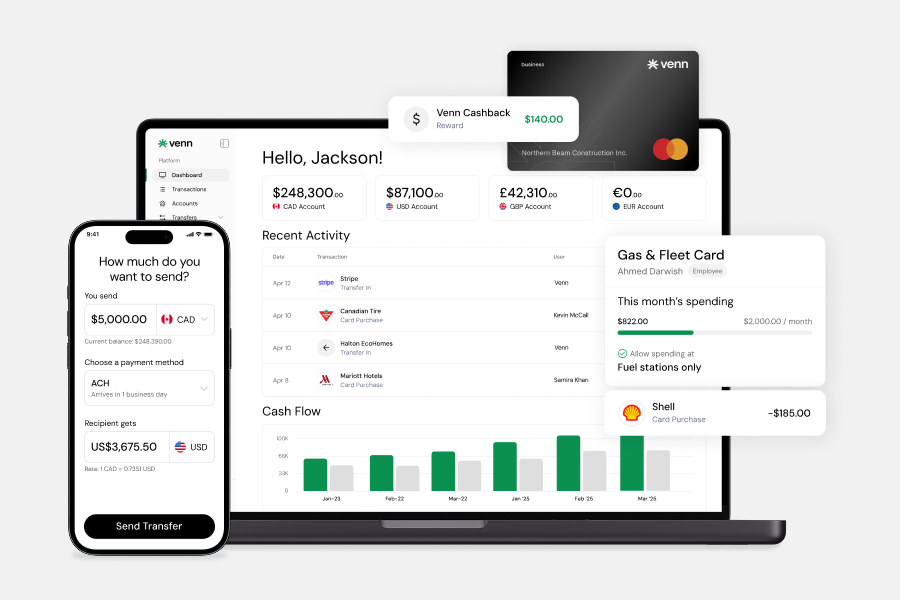

For Canadian businesses, virtual cards are digital-only payment methods that can be instantly issued and customized to support controlled, trackable spending across teams. Unlike traditional corporate cards, virtual cards offer more flexibility and granular control without needing to ship or manage physical inventory.

Instead of waiting for a plastic card to arrive or tracking down receipts after the fact, finance teams can issue virtual cards in seconds with predefined spend limits, expiry dates, and approved merchant categories. These cards are typically accessed through mobile wallets or browser-based platforms and are ideal for remote teams, distributed departments, or employees who don’t need permanent access to corporate funds.

From reconciling SaaS subscriptions to managing travel budgets or project-based spending, virtual cards are designed to support businesses that want faster control, real-time oversight, and tighter expense policies without adding overhead.

Why Virtual Cards Matter for Canadian Businesses

- They can be created and revoked instantly: Essential for controlling spend across growing teams or freelance contractors.

- They reduce fraud and unauthorized spend: Every transaction is tied to a specific user or use case.

- They support real-time tracking and automated reconciliation: Making month-end reporting faster and more accurate.

- They support multi-currency spend: Avoiding costly FX conversion fees when paired with CAD/USD/GBP/EUR accounts.

Venn’s virtual cards go a step further by offering true multi-currency support on a single card, 1% cashback with no FX markups, and native integrations with QuickBooks and Xero, enabling real-time reconciliation that finance teams can trust.

Who Should Use Virtual Cards? (Use Cases for Canadian Businesses)

Virtual cards aren’t just a modern payment method, they’re a strategic financial tool for Canadian businesses that need control, speed, and flexibility in how money moves across their teams.

Below are the key business profiles that benefit most from adopting virtual card infrastructure:

Startup CFOs Managing Fast-Moving Spend

For CFOs at early to growth-stage startups, spend often evolves faster than your policies can catch up. Whether it’s paying for ad campaigns, travel, or SaaS tools, virtual cards give you:

- Instant card issuance to get teams moving without operational delays.

- Merchant-specific controls to prevent spending outside of approved tools.

- Real-time transaction visibility for better burn rate tracking.

Why it matters: You maintain control without slowing down the team, and month-end becomes smoother with less manual reconciliation.

SMB Finance Teams Running Lean

Finance managers at small and mid-sized businesses are often responsible for more than just bookkeeping, they’re also enforcing policy, chasing receipts, and managing AP manually.

Virtual cards reduce that admin burden by:

- Automatically categorizing transactions and linking them to specific users or departments.

- Eliminating paper receipts through real-time digital logging.

- Reducing risk with temporary, project-based cards for contractors or events.

Why it matters: Virtual cards automate spend hygiene, freeing up finance to focus on planning and analysis, not cleanup.

Professional Services Firms & Agencies

Whether you’re a digital agency, consultancy, or software services firm, virtual cards streamline how your project teams spend:

- Allocate cards per client or campaign and set strict limits.

- Avoid FX fees on tools like Figma, Google Ads, or remote freelancers.

- Track billable spend by client or department to simplify recharges.

Why it matters: With Venn, agencies can operate globally without getting buried in spreadsheets or juggling multiple platforms for spend visibility.

Learn more about common use cases of virtual cards in our new blog here!

5 Business Advantages of Virtual Cards

For finance teams looking to modernize spend control, virtual cards offer more than convenience, they enable smarter, faster decisions by putting controls at the point of transaction. Below are five strategic advantages for Canadian businesses using virtual cards:

1. Instant Issuance & Real-Time Control

Virtual cards can be created and distributed in seconds, no printing, mailing, or waiting required. Finance teams can:

- Set granular spend limits

- Restrict cards to specific vendors or categories

- Pause or cancel instantly if misuse is suspected

Why it matters: You reduce risk while enabling employees to move fast, no shared cards, no waiting for the mailroom, no compliance gaps.

2. Real-Time Expense Visibility

Every transaction made on a virtual card is logged in real time. Combined with accounting integrations like QuickBooks or Xero, you get:

- Immediate GL coding

- Better forecasting and budget control

- Live dashboards for finance and operations

Why it matters: You eliminate the black box of mid-month spending and gain up-to-the-minute clarity on cash outflows.

3. Built-In Fraud Protection

Virtual cards aren’t exposed the way physical cards are, no card theft, no number skimming, no misuse if a staff member leaves. You can issue single-use cards, restricted by geography or merchant, and expire cards automatically.

Why it matters: You reduce fraud exposure without relying solely on employee compliance or reactive fraud claims.

4. Cleaner Month-End Reconciliation

Because each virtual card can be assigned to a person, team, or project, reconciling expenses is drastically simplified. Many businesses link cards directly to vendors (e.g. Meta Ads, Figma, Notion) for auto-categorization.

Why it matters: Finance spends less time chasing receipts or sorting through generic “corporate card” statements.

5. Optimized for Global Spend

Venn’s virtual cards support CAD, USD, GBP, and EUR, all on a single card. That means:

- No cross-border fees when paying from the right currency

- No FX surprises or delays

- Full compatibility with international vendors and platforms

Why it matters: You can operate like a global company without the legacy banking overhead or hidden FX costs.

5 Business Disadvantages of Virtual Cards

Virtual cards are a powerful tool, but they’re not without tradeoffs. Understanding the limitations helps Canadian finance teams set the right expectations, design better controls, and choose the right provider.

1. Merchant Acceptance Gaps

Some vendors, especially in-person or older B2B suppliers, don’t accept virtual cards. This is more common in:

- Utilities and government services

- Local trades or contractors

- Industries that still require physical POS terminals

Mitigation: Maintain one physical card for exceptions, and use bank transfers or EFTs (which Venn supports) where card acceptance is limited.

2. Device Dependency

Virtual cards typically live inside mobile wallets or browser-based apps. If an employee’s device dies, is lost, or has no internet access, the card becomes temporarily unusable.

Mitigation: Enable contactless support on mobile devices and ensure offline access where possible. Venn offers both Apple and Google Pay and also offers Interac e-Transfers and traditional EFTs for backup scenarios.

3. Change Management Required

Not all employees are immediately comfortable switching from personal cards or traditional reimbursement models. This can lead to low adoption or shadow spend.

Mitigation: Pair card rollout with training and a clear expense policy. Emphasize time saved and reduced out-of-pocket costs for employees. Venn allows card assignment without lengthy re-verification.

4. Platform Limitations (Fees, Visibility)

Not all virtual card platforms offer the same level of transparency or cost control. Some charge per-card fees, lack multi-currency support, or make it difficult to assign and track spend across teams.

Mitigation: Choose a provider with no per-card fees, multi-currency capabilities, and true accounting integration. Venn’s cards include all of this out of the box.

5. Audit Complexity for High-Volume Users

If a company issues hundreds of virtual cards across multiple departments or projects, spend tracking can become overwhelming without tight integration.

Mitigation: Use virtual cards in tandem with rules-based approval flows and GL-coded spend categories. Venn allows you to sync transactions directly to your accounting software for audit-ready compliance.

Virtual vs Physical Cards: Which Is Better for Your Business?

Virtual and physical cards both serve a role in modern business finance—but the key difference lies in speed, control, and visibility.

Here’s how they compare when evaluated through a finance leader’s lens:

Bottom line: Virtual cards offer better control and visibility for digital-first businesses, while physical cards may still be useful for specific in-person or legacy spend cases.

With Venn, you don’t have to choose, our platform supports both, letting you decide card-by-card how to issue and control team spend.

How Venn Makes Virtual Cards Work Better in Canada

Most virtual card providers promise control, speed, and visibility. But Venn goes further, solving the key limitations that hold other Canadian platforms back.

If you're managing multi-currency operations, reconciling team expenses, or simply trying to avoid legacy banking delays, Venn is purpose-built for you.

Here’s how we stand out:

Where competitors like Float or Loop fall short, by lacking USD/EUR accounts, forcing currency-specific cards, or delaying payments, Venn provides a truly unified spend infrastructure for Canadian businesses scaling globally.

Should Your Business Use Virtual Cards?

If you're a Canadian finance leader managing distributed teams, growing SaaS costs, or project-based spending, yes, virtual cards should be part of your stack.

They offer:

- Faster issuance than physical cards

- Better spend control and fraud protection

- Real-time reconciliation to reduce month-end headaches

- Flexibility for remote and global teams

But not all virtual cards are created equal. Many Canadian platforms limit you to CAD only, delay payments, or charge hidden fees.

Venn solves these gaps with:

- One card for CAD, USD, GBP, and EUR

- Real Canadian payment rails (EFTs, Interac, bill pay)

- 2% interest on all CAD/USD balances

- Seamless QuickBooks/Xero sync

- Unlimited cashback on local spend

- Same-day wire delivery

Finance leaders choose Venn because it delivers full control, without adding complexity.

Frequently Asked Questions About Virtual Cards for Canadian Businesses

Q: What is a virtual card used for in business?

A virtual card is a digitally generated payment card used to improve expense management, control budgets, and pay vendors. They are ideal for locking down SaaS subscriptions, managing digital ad spend, paying for team travel, and eliminating the need for complex employee reimbursements.

Q: Are virtual cards secure for business payments?

Yes, they are highly secure. Virtual cards are safer than physical cards because they are created with unique details, can be locked to a specific vendor or spending limit, and can be instantly deactivated in real-time if fraud is suspected. There is no physical card to be lost or stolen.

Q: Can I use virtual cards in Canada for multi-currency payments?

With many traditional providers, you are limited to CAD, often incurring high cross-border fees. However, modern platforms like Venn allow Canadian businesses to spend in multiple currencies (e.g., CAD, USD, EUR, and GBP) from a single virtual card, eliminating unnecessary FX fees when the card is funded in the right currency.

Q: Do virtual cards work with accounting software like QuickBooks or Xero?

Absolutely. Virtual cards offered by expense management platforms integrate directly with major accounting software like QuickBooks and Xero. This integration allows transactions and receipts to be pushed and coded in real time, dramatically simplifying reconciliation and month-end closing.

Q: What are the downsides of using virtual cards in a company?

The main downsides are: 1) Vendor Acceptance: Some older or smaller suppliers may not yet accept virtual cards, requiring an alternative payment method, and they are generally not accepted for in-person transactions like car rentals. 2) Employee Adaptation: Employees may need training to adapt to a digital-first expense process.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 5,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 5,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.