Venn vs CIBC - Best Bank Account for Canadian Businesses

Compare Venn vs. CIBC Business Banking. Discover which platform offers better fees, FX rates, and digital tools for Canadian businesses.

Ahmed Shafik

Co-founder

Trusted by 15,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

For Canadian businesses, the choice between traditional banking and modern financial platforms is no longer theoretical, it’s tactical.

Whether you're a founder tired of jumping between bank portals, or a finance lead managing cross-border vendors and FX reconciliations, the decision comes down to one core question: Do you want to stitch tools together, or use one platform that works out of the box?

That’s where the comparison between Venn and CIBC Business Banking comes in.

CIBC is a well-established institution offering conventional business accounts and services. But with limitations around fees, branch-based onboarding, and global payments, it can feel outdated, especially for modern, digitally fluent teams.

Venn, on the other hand, is built for Canadian businesses that want a full financial operating system. You get:

- Multi-currency accounts (CAD, USD, GBP, EUR)

- Corporate cards with uncapped 1% cashback

- 2% interest on USD/CAD balances, unlocking passive revenue for your business.

- AP, AR, global transfers, FX optimization, and accounting sync — all in one place

If you’re weighing Venn vs. CIBC, you've come to the right place.

Venn vs. CIBC: Side-by-Side Comparison

Let's take a closer look into some of the features that are avaliable to Venn and CIBC business banking users. Here’s how the two solutions differ across their most important features:

| Feature | Venn | CIBC Business Banking |

|---|---|---|

| Monthly Account Fee | Tiered: $0 (Essentials), $40 (Plus), $100 (Pro) | $6–$65+ depending on plan and balance |

| Multi-Currency Accounts | CAD, USD, GBP, EUR (included with all plans) | CAD and USD only; no GBP or EUR support |

| Corporate Cards | Multi-currency cards with 1% cashback and unlimited virtual cards | Credit cards available; limited cashback and FX flexibility |

| Accounts Payable (AP) | Automated workflows with built-in global payments | Manual payments or third-party tools required |

| Accounts Receivable (AR) | Invoicing, payment links, and credit card acceptance included | Limited — external invoicing systems required |

| Interest on Balances | 2% on CAD and USD balances | None on operating accounts |

| Interac e-Transfer® | Unlimited and free across all plans | Available; may incur per-transfer fees |

| FX & Global Transfers | 0.25%–0.45% FX markup; send to 200+ countries | 2.5%–3% FX markup via SWIFT network |

| Onboarding & Access | 100% online onboarding in under 10 minutes | Branch visit typically required for setup |

| Accounting Sync | Two-way sync with QuickBooks and Xero | CSV exports only; no direct integration |

What Is the Difference Between Venn and CIBC Business Banking?

If you’re comparing Venn vs. CIBC business banking, the most important distinction comes down to how each platform fits into your daily operations. Let’s compare some of the differences between the two providers.

CIBC is one of Canada’s Big 5 banks, offering traditional business accounts, credit products, and merchant services. It's a familiar name, but its infrastructure reflects legacy systems: paperwork-heavy onboarding, limited automation, and fragmented tools that often require external integrations to do basic financial management.

Venn, by contrast, was built from the ground up for Canadian businesses that operate online, across borders, and with lean finance teams. It offers an all-in-one financial operating system, meaning you can manage multi-currency accounts, corporate cards, global transfers, AP/AR, and expense automation all in one dashboard, without relying on multiple providers.

Here’s the core difference:

CIBC is a bank with online features. Venn is an online-first financial platform that replaces traditional business banking.

Where CIBC might offer separate USD accounts with high FX fees and manual transfers, Venn provides integrated, no-fee multi-currency accounts with transparent FX rates and automated vendor payouts all designed to scale with your business.

If your goal is to reduce friction, cut fees, and consolidate financial workflows, Venn offers a modern alternative to legacy business banking.

Feature: Business Accounts and Core Banking

When choosing between CIBC and Venn for managing your business’s day-to-day finances, the structure and flexibility of the core business account is foundational.

Venn

Venn offers fully integrated multi-currency accounts (CAD, USD, GBP, EUR) that act as your operational base, all accessible through a single login. These accounts come with no monthly fees on the Essentials plan, and every business gets unique account numbers for each currency, making it easy to send and receive local and international payments without extra conversion steps.

Beyond balances, these accounts are deeply integrated into the rest of Venn’s platform. That means you can trigger payments, pull bills from accounting tools, automate receivables, or issue corporate cards, all from the same system, with no need to log into external banking portals. From the mobile app, teams can access account funds, send transfers, and create new cards directly from their phones.

CIBC

CIBC’s business banking includes several types of chequing-style accounts, with pricing tiers based on monthly transaction volume. While CAD and USD accounts are available, they often come with monthly maintenance fees, e-Transfer limits, and tiered pricing for wire transfers or teller access.

CIBC does not support true multi-currency accounts. Businesses that operate in GBP or EUR must rely on costly wire transfers or third-party FX solutions, often at a markup of 2–3%. Each account is siloed from corporate cards, invoicing, or spend management, requiring additional tools and manual reconciliation.

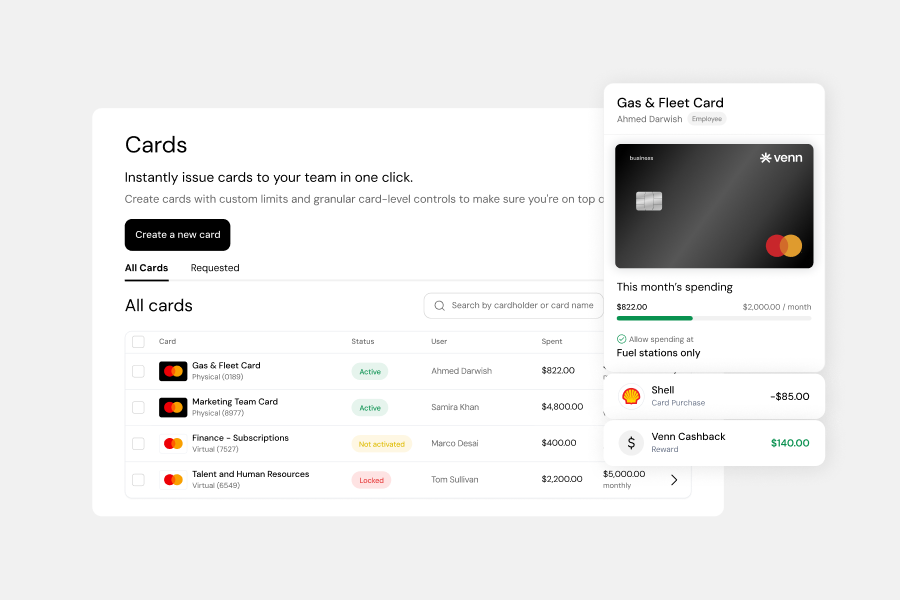

Feature: Corporate Cards for Business Expenses

Both Venn and CIBC offer business cards, but their approach and functionality differ dramatically.

Venn

Venn provides a single multi-currency corporate card that draws from your Venn account balances in CAD, USD, GBP, or EUR. The platform automatically selects the most relevant currency balance to avoid unnecessary FX conversions. Each card earns 1% cashback on all purchases with no minimum spend or points conversion.

Virtual and physical cards can be issued instantly, with real-time controls for spending limits, category restrictions, and approval workflows. Because cards are tied directly to your Venn balance, there’s no credit check or float period, you stay in control of your business spend in real time.

CIBC

CIBC offers a variety of business credit cards, typically tied to the business’s credit profile. While cashback or rewards are available, they are often limited to CAD spending and come with eligibility requirements or annual fees. Foreign transactions typically incur a 2.5% FX fee.

CIBC cards are separate from your business accounts, so you’ll need to manually reconcile card statements, apply for credit limits, and manage separate portals for issuing or managing cards. Approval times may also be slower, especially for new businesses or those without significant credit history.

Looking for a corporate card with no foreign transaction fees and automated controls? Venn's offering is a modern alternative.

Feature: Expense Management Automation & Tracking

Expense visibility and control are essential for managing team spending, whether via cards or reimbursement.

Venn

Venn centralizes all employee spending within the same platform as its accounts and cards. Real-time tracking, merchant-level detail, and receipt capture are built-in, and you can define approval chains per department, project, or team. Giving you a better way to manage your team's expense management.

Expenses automatically sync with QuickBooks or Xero, and recurring patterns can trigger automated rules for categorization or approval. This unified view of spend means less time reconciling, and more time optimizing cash flow.

CIBC

CIBC does not provide native expense management tools. While you can download transactions or integrate third-party tools, most businesses must rely on external software to handle approvals, receipt collection, and categorization. This creates fragmentation between banking and expense control, increasing admin time for finance teams.

If you're evaluating digital business banking solutions in Canada, automation is key, and this is where Venn leads.

Feature: Global Transfers & FX Functionality

International business requires more than just the ability to send a wire. Cost, speed, and currency flexibility matter.

Venn

Venn supports outbound transfers to 180+ countries in 30+ currencies, with local rails like ACH, SEPA, and Faster Payments. FX fees are as low as 0.25%, depending on your plan, and all rates are transparent within the platform.

Because accounts are already multi-currency, you can hold, convert, and send funds without moving money between providers. International vendors get paid faster, with fewer deductions.

CIBC

CIBC relies on the SWIFT network for most international payments, which means higher fees, slower settlement, and multiple intermediary banks. FX rates are typically marked up by 2–3%, and GBP/EUR payments may require pre-conversion or holding accounts, limiting flexibility.

Searching for the best bank for small business in Canada that supports global business? Compare FX fees and international support carefully.

Feature: Accounts Payable (AP) & Vendor Payments

Paying bills should be seamless, not spreadsheet-driven. Let’s compare the AP and vendor payment workflows between CIBC and Venn.

Venn

Venn pulls vendor bills directly from your accounting platform, categorizes them automatically, and lets you schedule or approve payments in one click. Whether it’s EFT, ACH, wire, or Interac e-Transfer®, Venn handles it all from within the same interface.

Customizable approval chains, auto-tagging, and status tracking give you full control without the manual coordination. Payments are tracked in real time, and matched automatically against invoices and accounting data.

CIBC

CIBC offers basic bill pay functionality, but it’s not built for finance automation. You’ll typically need to enter vendor details manually or use accounting software integrations for reconciliation. For teams processing dozens of vendor payments a week, this adds time and potential for error.

Businesses looking for a CIBC business banking login alternative that integrates AP directly into daily workflows may prefer Venn.

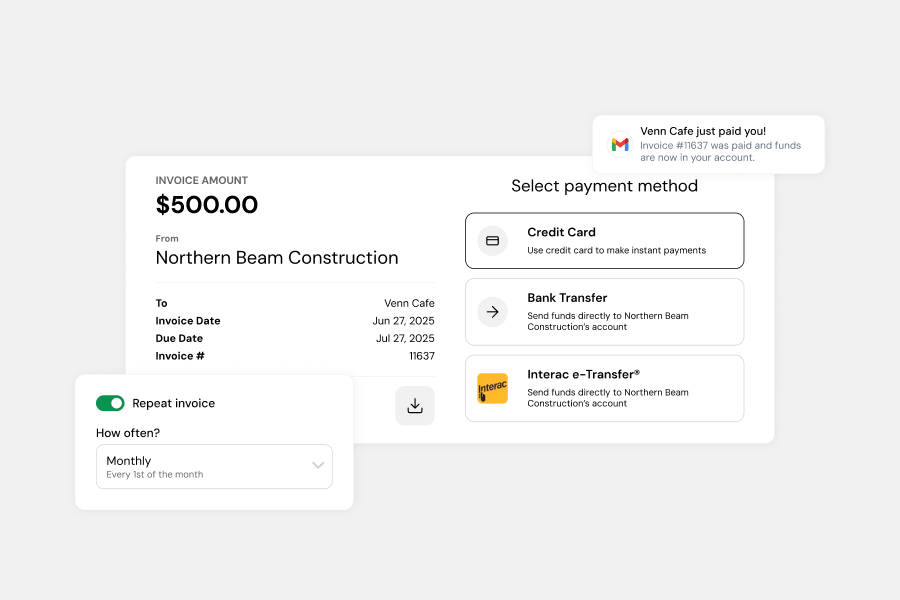

Feature: Invoicing & Accounts Receivable (AR)

Managing incoming payments is just as important as managing outgoing ones.

Venn

Venn includes a built-in invoicing feature that lets you issue multi-currency invoices, accept credit card or bank payments, and track payment status in one place. Businesses can pass on fees or absorb them, depending on workflow preferences.

The platform also syncs receivables into accounting tools and flags overdue invoices, giving you one system to manage both sides of your cash flow.

CIBC

CIBC does not offer invoicing or AR automation. Businesses must rely on third-party tools (like QuickBooks or FreshBooks) to send and manage invoices. Payments arrive separately and require manual matching. This can lead to lag times in reconciliation and reduced visibility.

Looking for a CIBC digital business banking alternative that integrates AR with payments and accounts? Venn provides a complete solution.

Feature: Accounting Integrations

Syncing your bank data with your accounting software shouldn’t require workarounds.

Venn

Venn offers 2-way sync with both QuickBooks Online and Xero, allowing real-time updates, categorization, and rule application across accounts, cards, and expenses. You can also apply custom tagging and audit trails for cleaner books.

The result? Fewer errors, no CSV uploads, and faster month-end close.

CIBC

CIBC provides basic transaction feeds to accounting software, but lacks categorization, automation, or rules-based sync. In many cases, businesses need to export CSV files or reconcile line items manually, especially if using additional tools like expense platforms or invoice software.

If you’re frustrated by the limitations of CIBC online business banking, Venn’s automation may offer the right fit.

Feature: Security, Compliance & Safeguarding

Both platforms operate within Canada’s financial regulatory framework, but their models differ.

Venn

Venn is registered as a Money Services Business (MSB) with FINTRAC and employs a safeguarding model where funds are held with tier-1 banks, but never lent out. Encryption, 2FA, and permission-based access are standard. All funds held with Venn are covered under CDIC protection up to $100,000.

Its infrastructure is purpose-built for modern financial workflows, with real-time monitoring and built-in audit logs across all user actions.

CIBC

CIBC is a Schedule I Canadian bank and a CDIC member. It provides traditional deposit protection and compliance controls, though it may be slower to innovate on real-time transparency or in-app controls.

For businesses that require frequent updates or customizable access, Venn may offer more agility without compromising compliance.

Feature: Customer Support & Onboarding

How fast you can get started, and how quickly you get help when needed, can define the user experience.

Venn

Venn offers fully online onboarding with approval often completed same-day. Support is available via live chat, email, and (on higher tiers) dedicated account managers. Most issues are resolved within hours, not days.

CIBC

CIBC onboarding may require in-person visits and document hand-offs. While support is available by phone or in-branch, wait times can be inconsistent, especially for small business clients not assigned to a dedicated advisor.

For businesses looking to avoid branch visits and streamline setup, Venn’s model aligns better with modern expectations for online business banking in Canada.

Pricing & Fees

Cost transparency is crucial when evaluating financial platforms. While CIBC’s business banking model is rooted in traditional tiered pricing, with monthly account fees, transaction limits, and FX markups, Venn offers a more predictable and modern pricing structure. Below is a side-by-side breakdown to help you compare account fees, international transfer costs, and foreign exchange rates.

| Feature | Venn | CIBC Business Banking |

|---|---|---|

| Monthly Account Fee | Essentials: $0 Plus: $40 Pro: $100 |

$6–$65+ depending on tier |

| Local Transfers (EFT/ACH) | Free on Plus & Pro $2 on Essentials |

Some included; overages $1.50–$2.50 |

| International Wires | $10 (Essentials) $8 (Plus) $6 (Pro) |

$15–$80 depending on destination |

| Foreign Exchange (FX) Fees | 0.25% (Pro) 0.35% (Plus) 0.45% (Essentials) |

2.5%–3% markup on average |

| Card Cashback | 1% cashback, no minimum spend | 0.5%–1%, often with annual fee or spend thresholds |

Venn: Strengths & Considerations

Pros:

- Integrated Multi-Currency Accounts: Seamless management of CAD, USD, GBP, and EUR funds from a single platform, eliminating the need for third-party FX tools or multiple bank accounts.

- Customizable Corporate Cards and Expense Management: Issue physical or virtual cards with custom spend limits and approval workflows — tied directly to Venn accounts.

- 1% Cashback with No Minimum Requirements: Earn cashback on all card spend with no minimum thresholds or tier requirements.

- Automated Expense Management: Built-in receipt capture, categorization rules, and multi-level approval flows simplify tracking and reconciliation.

- Robust Accounts Payable Automation: Automate vendor payments with global methods like EFT, ACH, SEPA, and Interac e-Transfers®.

- 2% interest on CAD/USD balances: Earn passive revenue on your business balances, no minimums or lock-in periods.

- QuickBooks and Xero Integrations: Two-way sync with leading accounting platforms ensures accurate, real-time financial records.

- Competitive FX and Global Transfers: Low FX fees (as low as 0.25%) and support for sending funds in over 30 currencies to 180+ countries.

- CDIC Deposit Insurance: Eligible business deposits are insured up to $100,000 under federal protection.

- Transparent Pricing: Simple, flat-fee pricing across all tiers with no hidden charges and clearly disclosed foreign exchange rates.

- Invoicing and Receivables: Send multi-currency invoices and accept credit card or bank payments directly within Venn.

- Fully Digital Onboarding: No branch visits or paper forms required to get started.

Cons:

- While Venn is rapidly maturing, some businesses may prefer the familiarity of traditional banks or legacy financial institutions, especially when it comes to lending products or in-person support.

CIBC Business Banking: Strengths & Considerations

Pros:

- Established Banking Brand: As one of Canada’s Big 5 banks, CIBC is trusted and widely recognized.

- Branch Access Nationwide: In-person service available across Canada, ideal for businesses that prefer face-to-face banking.

- Lending and Credit Options: Offers small business loans, lines of credit, and credit cards to support growth.

- CDIC Deposit Insurance: Eligible business deposits are insured up to $100,000 under federal protection.

- Comprehensive Legacy Services: Includes access to merchant terminals, treasury management, and other traditional offerings.

Cons:

- Limited Multi-Currency Options: Only CAD and USD accounts available; no support for holding GBP or EUR balances natively.

- Higher FX Fees: Markups on foreign exchange and international wires typically range between 2% and 3%.

- Manual Onboarding and Admin: Account setup and service changes often require in-branch visits and paperwork.

- No Built-in Spend or AP Automation: Lacks integrated tools for managing employee spending, payables, or AR workflows.

- Fragmented Experience: Requires juggling multiple platforms for cards, FX, accounting, and expense management.

- Tiered and Add-On Fees: Monthly account fees, per-transaction charges, and premium service tiers can drive up costs.

Which Platform is Right for Your Business?

Ultimately, choosing between Venn and CIBC depends on the type of financial infrastructure your business needs.

If you're looking for a modern, all-in-one financial platform that combines business banking, multi-currency accounts, corporate cards, expense automation, and global payments, Venn is a clear fit. It's purpose-built for growing Canadian businesses that want to move fast, manage finances digitally, and reduce manual reconciliation across disconnected tools.

On the other hand, if your business requires access to lending, branch-based services, or you're already entrenched in a traditional banking relationship, CIBC may offer the familiarity and range of credit products you need, albeit with tradeoffs in speed, flexibility, and digital automation.

For small businesses and scaling teams that value efficiency, transparency, and global reach, Venn offers a compelling alternative to the status quo.

Ready to Modernize Your Business Banking?

Venn helps Canadian companies take control of their financial operations, from payables to payroll, cards to currencies. Get started in minutes and explore how Venn can simplify your business banking experience.

Key Takeaways: Venn vs. CIBC Business Banking

- All-in-One vs. Traditional Banking: Venn offers a modern, all-in-one financial platform with integrated banking, multi-currency accounts, global payments, AP/AR automation, and corporate cards. CIBC, as a traditional bank, provides solid foundational services but requires layering multiple tools for full functionality.

- Multi-Currency Advantage: Venn supports CAD, USD, GBP, and EUR in one platform with seamless switching and low FX rates. CIBC supports only CAD and USD with higher FX markups and no unified interface for global currency management.

- Corporate Cards and Cashback: Venn offers virtual and physical cards with 1% cashback and no minimum spend. CIBC's business credit cards offer lower cashback rates with tiered conditions and annual fees.

- Global Payment Infrastructure: Venn enables fast, low-cost transfers to 200+ countries in 30+ currencies. CIBC relies on slower, higher-cost SWIFT transfers for international payments.

- Fees and Transparency: Venn’s pricing is transparent with flat monthly tiers and clear FX fees (as low as 0.25%). CIBC's fees vary by account type, with multiple hidden charges for wires, transfers, and cash management.

- Speed of Setup: Venn offers fully digital onboarding, often same-day. CIBC may require branch visits and longer approval timelines.

- Business Fit: Venn is ideal for startups, SMBs, and globally-oriented businesses looking for automation and modern tools. CIBC suits businesses preferring a traditional banking relationship or that already have other products with the bank.

Frequently Asked Questions (FAQs)

Q: What is the difference between Venn and CIBC business banking?

Venn is a modern financial operating system built for digital businesses, offering integrated multi-currency accounts, automated expense management, corporate cards, and payment tools in a single platform. CIBC provides traditional business banking services, including an extensive branch network, dedicated lending services, and various investment products, but it typically lacks the built-in expense automation and foreign exchange efficiency of modern fintech platforms.

Q: Which platform has better foreign exchange rates — Venn or CIBC?

Venn offers significantly better foreign exchange rates and greater transparency. Venn's FX fees start as low as 0.25% on its premium plan for all conversions. In contrast, CIBC and other large banks typically apply an undisclosed FX markup that ranges from 2% to 3% on international transfers and debit card currency conversions, making Venn substantially more cost-effective for businesses that transact globally.

Q: Does CIBC offer multi-currency business accounts like Venn?

CIBC offers Canadian dollar (CAD) accounts and a dedicated U.S. Dollar (USD) Current Account. However, it does not provide full, integrated multi-currency operating accounts for major international currencies like the British pound (GBP) or the Euro (EUR). Venn, by contrast, provides native, integrated accounts for CAD, USD, GBP, and EUR, allowing businesses to hold, send, and receive funds in these currencies like a local business, all from one digital dashboard.

Q: Does Venn offer lending or lines of credit like CIBC?

No. This is a key difference in service scope. CIBC is a full-service bank and offers a comprehensive range of borrowing solutions, including small business loans, lines of credit, and commercial mortgages. Venn focuses on core financial operations, payments, and spend management, and it does not currently provide any lending or credit products.

Q: How does onboarding differ between Venn and CIBC?

The onboarding process is a major differentiator. Venn offers a fully digital application and verification process, allowing most businesses to get approved and begin operating their new account and cards within one business day, with no need for in-person branch visits or paper documents. CIBC, while offering an online application, often requires follow-up paperwork or in-person verification steps to open or make changes to business accounts.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 15,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 15,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.