Top Ramp Competitor for Canadians: 8 Best Alternatives for 2026

Discover the best Ramp competitor for Canadians. Compare 8 leading alternatives designed for Canadian businesses seeking secure, efficient banking solutions.

Trusted by 10,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

Ramp is one of the most popular spend management platforms in the US, but Canadian businesses face a fundamental problem: Ramp requires a US entity, a US bank account, and US credit underwriting. No Canadian entity support. No CAD accounts. No access to local payment rails. For Canadian operations, these are not minor inconveniences; they are dealbreakers that cut you off from the platform entirely.

The cost of working around these restrictions adds up fast. You are looking at 2-3% FX markups on every international transaction, days-long wire transfer delays, inability to pay Canadian vendors efficiently, and manual workarounds that scale poorly as your business grows. Layer on the compliance headaches around GST/HST reporting and disconnected accounting workflows, and that "modern" US platform suddenly feels like a step backward from your current setup.

This guide provides what is missing from US-centric comparisons: a detailed analysis of eight Ramp alternatives that actually work for Canadian businesses. We examine each platform's pricing, features, Canadian-specific capabilities, and integration options through the lens of what matters to Canadian operations. Some are purpose-built for the Canadian market. Others are global platforms with varying degrees of Canadian support. All offer different approaches to solving the spend management challenge.

Whether you need multi-currency accounts to handle cross-border operations, lower FX rates to protect your margins, or seamless QuickBooks integration to keep your books clean, this guide will help you find the right Ramp alternative for your Canadian business. Let's start by understanding why Ramp's limitations matter more than most reviews acknowledge.

Why Canadian Businesses Need Ramp Alternatives

Ramp's success in the US market makes its Canadian limitations particularly frustrating. The platform excels at automated expense management, intelligent spend controls, and generous cashback rewards, but none of that matters if you cannot access it properly. While Ramp has recently introduced limited Canadian access, the restrictions remain significant for most Canadian businesses.

Ramp's Canadian Restrictions

Ramp now offers a limited Canadian program, but the fine print tells a different story. The program excludes businesses in Quebec and Saskatchewan entirely. It requires account minimums that put it out of reach for many SMBs. Most critically, all transactions settle in USD only, meaning every Canadian dollar payment triggers a currency conversion. For businesses that operate primarily in CAD, this creates constant, unavoidable FX exposure on everyday spending.

Currency and FX Exposure

Even if you qualify for Ramp's Canadian program, running Canadian operations through a USD-denominated platform creates expensive friction. Without CAD accounts, every Canadian vendor payment requires currency conversion at 2-3% markups. Without access to Interac e-Transfer® or EFT, you are forced into expensive wire transfers or checks. Without Canadian credit underwriting, your Canadian employees may struggle to get approved for cards. These costs compound quickly, often eliminating any savings from Ramp's rewards program.

Tax Handling Gaps

Ramp's tax engine is built around US sales tax, which operates on fundamentally different rules than Canada's GST/HST framework. Managing GST/HST reporting becomes a manual exercise when your spend platform does not understand Canadian tax requirements. Input tax credits, provincial sales tax variations, and HST filing deadlines all require manual rework outside the platform. For finance teams already stretched thin, this creates hours of unnecessary reconciliation work every reporting period.

Bill Pay and ACH Limitations

Ramp cannot support ACH payments for Canadian entities. Canadian businesses using Ramp can only send payments via EFT, which takes approximately 7 days to settle. Compare that to platforms built for the Canadian market, where free EFT and ACH transfers settle in 1-2 business days. For businesses paying vendors on tight timelines, a week-long settlement window creates cash flow complications and strains supplier relationships.

ERP Limitations

Ramp does not support NetSuite for Canadian entities, a significant gap for mid-market businesses that rely on NetSuite as their core ERP. This means Canadian teams cannot take advantage of Ramp's automated sync and must instead export data manually, creating reconciliation delays and increasing the risk of errors. For growing Canadian businesses, these inefficiencies represent real constraints on scalability.

Key limitations for Canadian users:

• Limited Canadian access that excludes Quebec and Saskatchewan, requires account minimums, and settles in USD only

• No Canadian dollar accounts or local banking infrastructure

• No interest on holding balances

• Limited or no support for Interac e-Transfer®, a critical payment method in Canada

• Higher FX fees on cross-border transactions and currency conversions (2-3%)

• No Canadian credit underwriting, making card access difficult or impossible

• US sales-tax-based tax engine that requires manual GST/HST rework

• No ACH support for Canadian entities; EFT only with approximately 7-day settlement

• No NetSuite support for Canadian entities

• Lack of integration with Canadian payroll, tax, and compliance workflows

• Slower payment processing for domestic Canadian vendors

• Limited customer support during Canadian business hours

The good news is that the market has responded to these gaps. Several platforms now offer robust Canadian support or were built specifically for Canadian businesses. Many deliver features that match or exceed what Ramp provides in the US market, while adding capabilities that Canadian operations actually need. The challenge is understanding which platform aligns with your specific requirements.

Quick Comparison: Top Ramp Competitors for Canadian Businesses

Before diving into detailed reviews, this comparison table highlights the most critical features for Canadian businesses. We've focused on the factors that directly impact your operations: account currencies, card rewards, FX rates, Canadian payment support, and transparent pricing structures.

Note that accessibility doesn't equal optimization. While all these platforms serve Canadian businesses in some capacity, they vary dramatically in their depth of Canadian features, cost structures, and practical usability. Some excel as complete financial operating systems. Others specialize in specific areas like expense tracking or AP automation. Understanding these differences upfront will help you focus on the platforms that match your priorities.

The 8 Best Ramp Competitors for Canadian Businesses

Each platform in this review was selected based on specific criteria: accessibility to Canadian businesses, feature depth, pricing transparency, and ability to address Canadian operational needs. Some emerged from the Canadian market with deep local expertise. Others are global platforms that have invested in Canadian capabilities.

We've structured each review consistently to enable direct comparisons. You'll find an overview of the platform's strengths, detailed feature lists, Canadian-specific capabilities, transparent pricing information, and clear use case recommendations. This approach lets you evaluate options based on your specific requirements rather than generic feature comparisons.

1. Venn: All-in-One Business Banking and Spend Management for Canadian Companies

Best for: Canadian SMBs that need multi-currency accounts, corporate cards, AP automation, and accounting integration in one platform.

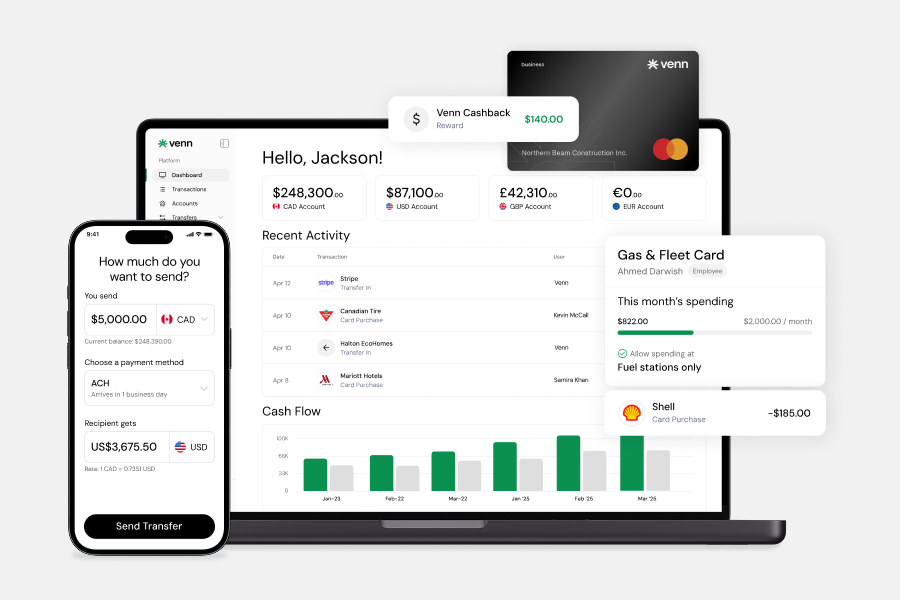

Venn represents a fundamentally different approach to the Ramp alternative question. Rather than simply replicating Ramp's spend management features, Venn built a complete financial operating system designed specifically for Canadian businesses. The platform combines business banking, corporate cards, expense management, invoicing, and AP automation in one unified system. As a registered Payment Service Provider (PSP) that is fully compliant with the Retail Payment Activities Act (RPAA), Venn meets the highest standard of Canadian financial regulation for platforms in its category.

The Canadian-first design philosophy shows in every feature. Real CAD and USD accounts with local banking rails mean you can receive payments, pay vendors, and manage cash flow without constant currency conversions. The lowest FX rates in Canada (0.25% over market)* protect your margins on international transactions. Unlimited free Interac e-Transfer® eliminates the wire transfer fees that plague other platforms.

Where Venn truly differentiates is in its pricing model and feature accessibility. The per-account pricing (not per-user) means growing teams do not face escalating costs. The 1% unlimited cashback applies from your first dollar spent, not after hitting arbitrary minimums. Multi-currency cards automatically charge the appropriate currency account, eliminating unnecessary conversions. These design decisions reflect a deep understanding of how Canadian businesses actually operate.

The integration capabilities complete the value proposition. Two-way sync with QuickBooks and Xero means your books stay accurate in real-time. Automated receipt capture and expense categorization eliminate manual data entry. AP automation with approval workflows streamlines vendor payments. Support for Pre-Authorized Debits (PADs) also makes Venn compatible with Canadian payroll platforms and recurring billing workflows. For Canadian businesses tired of juggling multiple disconnected tools, Venn offers genuine consolidation without compromise.

Key Features:

• Real CAD, USD, GBP, and EUR accounts with local banking infrastructure

• 1% unlimited cashback on all corporate card spend (no minimums or caps)

• Lowest FX rates in Canada at 0.25% over market

• Free unlimited Interac e-Transfer®, plus support for ACH, EFT, SEPA, and UK Faster Payments

• Multi-currency corporate cards that automatically pay from the currency you're spending in

• Built-in AP automation, invoicing, and expense management with OCR receipt capture

• Two-way sync with QuickBooks and Xero for automated reconciliation

• Real-time spend controls, approval workflows, and budget management

• Send payments to 180+ countries in 36+ currencies

• $6-10 global wires (vs $30+ at traditional banks)

• 2% interest on CAD and USD balances with no minimums

• 24/7 online support with Canadian business hours coverage

Canadian-Specific Advantages:

• Purpose-built for Canadian businesses with full CAD support

• Real Canadian bank accounts through Peoples Trust Company partnership

• Real US bank accounts with ACH send/receive capabilities (rare in Canada)

• Compliance with Canadian regulations and CDIC protection on funds

• No FX fees when receiving payments from Stripe, Shopify, or PayPal in USD

• GST/HST-ready reporting and multi-entity support

• No per-user fees, making it more affordable as teams grow

Pricing:

• Essentials: $0/month

• Plus: $29/month

• Pro: $99/month

• Pricing is per account, not per user

Venn eliminates the need for multiple disconnected tools by combining banking, cards, payments, and accounting in one platform. For Canadian businesses frustrated by Ramp's lack of Canadian support or tired of juggling traditional banks with separate expense tools, Venn offers a complete, modern alternative that actually saves money while adding capabilities.

2. Brex: US-Focused Spend Management with Limited Canadian Support

Best for: US-based startups with Canadian subsidiaries or operations that need US-centric spend controls.

Brex occupies a similar space to Ramp in the US market, offering corporate cards, expense management, and spend controls for fast-growing companies. The platform has earned recognition for its rewards program, real-time controls, and founder-friendly underwriting that doesn't require personal guarantees.

For Canadian businesses, Brex presents familiar challenges. The platform primarily serves US entities and offers USD accounts only. Any Canadian operations require currency conversions at standard 2-3% markups. Without access to Canadian banking rails, paying local vendors becomes expensive and slow. The lack of CAD support means constant FX exposure on everyday transactions.

Where Brex differentiates from Ramp is in its broader financial product suite and rewards flexibility. The points-based system offers more redemption options than pure cashback. The platform also provides cash management accounts and vendor payment capabilities. But these advantages matter less when the fundamental infrastructure doesn't support Canadian operations efficiently.

Key Features:

• Corporate cards with points-based rewards program

• Spend management with real-time controls and approval workflows

• Expense tracking and automated receipt matching

• Integration with QuickBooks, Xero, NetSuite

• Vendor payment capabilities

• Travel booking and management tools

• Cash management accounts (USD)

Limitations for Canadian Businesses:

• No CAD accounts or Canadian banking rails

• 2-3% FX fees on currency conversions

• Requires US entity for full access to features

• No Interac e-Transfer® support

• Limited Canadian customer support

Pricing:

• Essentials: Free

• Premium: $49/month

• Enterprise: Custom pricing

3. BILL: AP Automation with Vendor Payment Focus

Best for: Businesses that prioritize accounts payable automation and vendor payment workflows over corporate cards.

BILL (formerly Bill.com) takes a different approach to spend management by focusing intensely on accounts payable automation. The platform excels at digitizing the entire vendor payment workflow: invoice capture, approval routing, payment execution, and reconciliation. For businesses drowning in paper invoices and manual approval processes, BILL offers genuine efficiency gains.

The platform's strength in AP automation comes with limitations elsewhere. BILL offers no corporate card program, minimal expense management features, and limited support for employee spending. The US-centric design means Canadian businesses face higher fees for international payments and limited CAD functionality.

BILL works best as a specialized tool rather than a comprehensive platform. If your primary pain point is vendor payment efficiency and you're comfortable using separate solutions for cards and expenses, BILL can be valuable. But it's not a true Ramp alternative—it's a complementary tool that solves one specific part of the spend management puzzle.

Key Features:

• AP automation with invoice capture and approval workflows

• Vendor payment via ACH, check, or international wire

• Integration with QuickBooks, Xero, NetSuite, and other accounting platforms

• Multi-level approval workflows

• Payment scheduling and recurring payments

• Vendor management and 1099 tracking (US-focused)

Limitations for Canadian Businesses:

• Limited CAD support and Canadian banking integration

• No corporate card program

• Higher fees for international/cross-border payments

• US-centric features (1099 tracking, US bank account focus)

• No expense management or employee card issuance

Pricing:

• Essentials: $45/month

• Team: $55/month

• Corporate: $89/month

• Enterprise: Custom pricing

4. Airbase: Mid-Market Spend Management Platform

Best for: Mid-market companies with complex approval workflows and multi-department spend needs.

Airbase positions itself as the enterprise-grade answer to Ramp, with deeper procurement workflows, more granular controls, and robust reporting capabilities. The platform combines corporate cards, vendor payments, and expense reimbursements with sophisticated approval routing and spend policies.

For Canadian businesses, Airbase presents familiar challenges amplified by its enterprise focus. The platform is USD-only, lacks Canadian banking integration, and charges standard FX fees. The custom pricing model typically means higher costs than transparent alternatives. The complexity that serves large organizations becomes overhead for smaller teams.

Airbase makes sense for Canadian subsidiaries of US companies that need to align with parent company processes. For independent Canadian businesses, especially SMBs, the platform offers more complexity than value. The lack of Canadian infrastructure combined with enterprise pricing makes it an impractical choice for most Canadian growth companies.

Key Features:

• Virtual and physical corporate cards

• Procurement and approval workflows

• Vendor payment and invoice management

• Expense reimbursement tracking

• Real-time spend analytics and reporting

• Integration with major accounting platforms

• Multi-entity and department support

Limitations for Canadian Businesses:

• USD-only accounts

• Custom pricing (typically higher cost)

• No Canadian banking rails or CAD support

• 2-3% FX fees on conversions

• Designed for mid-market, may be overkill for SMBs

Pricing:

• Custom pricing based on company size and needs

5. Navan: Travel and Expense Management Combined

Best for: Companies with significant travel budgets that want integrated travel booking and expense management.

Navan (formerly TripActions) addresses a specific subset of spend management: business travel and related expenses. The platform combines corporate travel booking with expense tracking, creating efficiencies for companies where travel represents a major budget category. Policy enforcement happens at booking, not after the fact.

The travel focus means Navan isn't trying to be a complete spend management platform. There are no business accounts, limited AP automation, and the expense management features center on travel-related spending. Multi-currency support exists for international travel, but not for general business operations.

Canadian businesses with extensive travel programs might find value in Navan's specialized approach. But it's not a Ramp replacement—it's a travel management platform with some expense features. You'll still need separate solutions for banking, vendor payments, and non-travel expense management.

Key Features:

• Corporate travel booking (flights, hotels, car rentals)

• Travel policy enforcement and approval workflows

• Expense management and receipt capture

• Travel rewards program

• Multi-currency support for international travel

• Integration with accounting platforms

• Duty of care and travel tracking features

Limitations for Canadian Businesses:

• Travel-focused, not a full spend management platform

• No business banking or multi-currency accounts

• Limited AP automation

• Custom pricing can be expensive

• 2-3% FX fees on currency conversions

Pricing:

• Custom pricing based on travel volume and features

6. Expensify: Receipt Tracking and Reimbursement Platform

Best for: Small teams that need simple receipt tracking and employee reimbursement workflows.

Expensify pioneered mobile receipt capture and simplified expense reporting, making it a popular choice for small teams and individual professionals. The platform's strength lies in its simplicity: snap a photo, create a report, get reimbursed. For basic expense tracking needs, it remains effective.

However, the spend management landscape has evolved significantly since Expensify's launch. Modern platforms offer integrated corporate cards, real-time controls, and automated reconciliation that go far beyond receipt scanning. Expensify has added the Expensify Card, but it lacks the sophisticated controls and rewards programs of dedicated platforms.

For Canadian businesses evaluating Ramp alternatives, Expensify feels dated and limited. It solves the narrow problem of expense reporting but doesn't address broader financial operations. The per-user pricing model becomes expensive at scale. Most importantly, it lacks the banking, multi-currency, and automation features that modern businesses need.

Key Features:

• Mobile receipt scanning and OCR

• Expense report creation and approval

• Employee reimbursement processing

• Expensify Card with cashback

• Integration with QuickBooks and Xero

• Mileage tracking

• Basic corporate card controls

Limitations:

• Limited corporate card functionality compared to dedicated platforms

• No business banking or multi-currency accounts

• Basic AP automation

• Per-user pricing adds up for larger teams

• Limited Canadian-specific features

Pricing:

• Track: $5/user/month

• Submit: $9/user/month

• Collect: $18/user/month

7. SAP Concur: Enterprise Expense and Travel Management

Best for: Large enterprises with complex, multi-region expense and travel management needs.

SAP Concur represents the enterprise end of the expense management spectrum. As part of the SAP ecosystem, Concur offers deep integration with ERP systems, sophisticated policy engines, and global capabilities that large organizations require. The platform handles complex approval hierarchies, multi-entity structures, and compliance requirements.

For Canadian SMBs looking for Ramp alternatives, Concur is almost certainly overkill. The platform requires significant implementation effort, ongoing administration, and enterprise-level budgets. The feature depth that serves thousand-employee organizations becomes complexity that slows down agile teams.

Concur makes sense for large Canadian enterprises or Canadian divisions of multinationals that need to align with global processes. For growing Canadian businesses seeking modern, accessible spend management, platforms like Venn offer superior value with dramatically lower complexity and cost.

Key Features:

• Enterprise expense management

• Corporate travel booking and management

• Multi-currency and multi-entity support

• Policy enforcement and compliance

• Integration with SAP and other ERP systems

• Advanced reporting and analytics

• Audit and compliance tools

Limitations for Canadian Businesses:

• Enterprise pricing (expensive for SMBs)

• Complex implementation and setup

• No business banking or AP automation

• Designed for large organizations, not agile SMBs

• Requires dedicated admin resources

Pricing:

• Custom enterprise pricing

How to Choose the Right Ramp Alternative for Your Canadian Business

Choosing the right spend management platform isn't just about comparing feature lists. The best solution aligns with your business model, operational complexity, and growth trajectory. Canadian businesses face additional considerations that US-focused evaluation guides miss entirely.

Start with a honest assessment of your needs. Do you need a complete financial operating system that handles banking, cards, and payments? Or are you looking for a specialized tool to augment existing systems? Companies frustrated by disconnected tools and manual processes typically benefit more from comprehensive platforms like Venn. Those with established systems might prefer point solutions for specific pain points.

Currency exposure dramatically impacts platform selection. If your business operates exclusively in CAD with minimal international activity, a Canadian-focused solution like Float might suffice. But most growing businesses deal with USD suppliers, international customers, or cross-border operations. Platforms offering true multi-currency accounts save 2-3% on every foreign transaction compared to those requiring constant conversions.

Total cost of ownership extends far beyond monthly subscription fees. Per-user pricing models that seem reasonable at 5 employees become expensive at 50. Hidden transaction fees, FX markups, and wire transfer charges compound quickly. A platform with transparent per-account pricing and minimal transaction fees often proves more economical, especially as transaction volumes grow.

Integration capabilities determine operational efficiency. Manual data entry between disconnected systems creates errors and consumes valuable time. The best platforms offer real-time, two-way sync with QuickBooks and Xero, automated receipt capture, and approval workflows that eliminate busy work. Consider not just current integration needs but how those needs will evolve as you scale.

Key Factors to Evaluate:

• Multi-currency support: Do you need CAD, USD, and other currency accounts, or is CAD sufficient?

• Canadian banking rails: Does the platform support Interac e-Transfer®, EFT, and other local payment methods?

• FX rates: What are the actual markups on currency conversions, not just advertised rates?

• Card rewards: Are there cashback or rewards programs, and what are the earning thresholds?

• Pricing model: Is it per user, per account, or transaction-based? What are the hidden fees?

• Accounting integration: Does it sync seamlessly with your existing QuickBooks or Xero setup?

• AP automation: Can you automate vendor payments, invoicing, and approval workflows?

• Support: Is there Canadian customer support during your business hours?

• Compliance: Does the platform meet Canadian regulatory requirements and offer CDIC protection?

• Scalability: Will the platform grow with your business without requiring a complete migration?

Why Venn Is the Best Ramp Alternative for Canadian Businesses

After examining eight different platforms, clear patterns emerge. Most fall into two categories: US-focused platforms that treat Canadian businesses as afterthoughts, or narrow point solutions that solve one problem while creating others. Venn stands apart by delivering a complete financial operating system designed specifically for Canadian businesses.

The difference starts with infrastructure. Venn provides real Canadian and US bank accounts with local banking rails in each market. This is not just convenient; it is transformative. Receive USD payments without conversion. Pay Canadian vendors with free Interac e-Transfer®. Hold multiple currencies without constant FX exposure. These capabilities that Ramp cannot offer become the foundation for efficient operations.

The platform's comprehensiveness eliminates the tool sprawl that plagues growing businesses. Instead of separate subscriptions for banking, cards, expenses, invoicing, and payments, Venn consolidates everything. The 1% unlimited cashback from dollar one beats competitors that require high spending minimums. The lowest FX rates in Canada (0.25%)* protect margins on every international transaction. Per-account pricing means you do not get penalized for growing your team.

Venn's Canadian foundation shows in countless details that matter. As a registered Payment Service Provider (PSP) that is fully compliant with the Retail Payment Activities Act (RPAA), Venn meets the highest regulatory standard for financial technology platforms in Canada. GST/HST reporting that actually works. Integration with Canadian accounting workflows. Deposits eligible for CDIC deposit insurance up to applicable limits. Support during Canadian business hours. These are not features bolted on for market expansion; they are core to how the platform operates.

Most importantly, Venn scales with your business. Start with free Essentials for basic banking and cards. Upgrade to Plus ($29/month) when you need automation and advanced controls. Move to Pro ($99/month) for multi-entity support and premium features. At each stage, you get more capability without migration headaches or learning new systems.

What Makes Venn Different:

• Real CAD, USD, GBP, and EUR accounts with local banking infrastructure

• Lowest FX rates in Canada at 0.25% (vs 2-3% at banks and most competitors)

• 1% unlimited cashback with no spend minimums or caps

• Free unlimited Interac e-Transfer®, the only fintech in Canada to offer this

• Multi-currency cards that automatically use the currency you're paying in

• Complete AP automation, invoicing, and expense management built-in

• Two-way sync with QuickBooks and Xero for real-time reconciliation

• Per-account pricing, not per-user, making it affordable as teams grow

• 2% interest on CAD and USD balances with no minimums

• Real US accounts with ACH send/receive capabilities (rare in Canada)

• $6-10 global wires vs $30+ at traditional banks

• CDIC protection and Canadian regulatory compliance

For Canadian businesses evaluating Ramp alternatives, Venn offers the most complete, cost-effective, and Canadian-optimized solution available. Whether you're a startup managing your first international payments or a scaling SMB looking to consolidate financial tools, Venn delivers the platform you need to operate efficiently both domestically and globally.

Learn more about Venn or sign up for your Venn account to get started today.

*Based on published FX rates as of 2026. Rates may vary. See venn.ca/pricing for current rates.

FAQs About Ramp Alternatives for Canadian Businesses

Q: Can Canadian businesses use US platforms like Ramp directly, and what is the compliance barrier?

Yes now that Ramp has expanded to Canada you are able to open a Ramp

Q: What is the main advantage of choosing a Canadian-built platform over a US-centric platform?

Canadian-built platforms offer native integration with the local financial ecosystem. This includes real Canadian bank rails (Interac e-Transfer®, EFT, PADs), Canadian credit underwriting, local GST/HST compliance, and support during Canadian business hours, eliminating the friction and workarounds of US-centric systems.

Q: How much can Canadian businesses save on FX fees using a platform like Venn versus traditional banks?

The savings are substantial. Traditional banks charge typical FX markups of 2-3%, while platforms like Venn charge as low as 0.25%. For a business with $100,000 in annual international transactions, this difference translates to a saving of approximately **$2,750 per year** in fees.

Q: Do I need to close my existing bank account to switch to a platform like Venn?

No. Most modern platforms, including Venn, are designed to complement traditional banking. Many businesses maintain their existing bank account for specific needs (like loans) while using platforms like Venn for daily operations, international payments, expense management, and superior accounting automation.

Q: Are funds secure with platforms like Venn, and what about CDIC insurance?

Yes. Venn is a registered Payment Service Provider (PSP) that partners with Tier 1 Canadian banking institutions. Your eligible customer funds are held in designated trust accounts and are protected under CDIC insurance up to $100,000, ensuring the same level of security as a traditional bank.

---

**Disclaimer:** This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 10,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 10,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.