Profit First Accounts: How to Structure and Manage Them in Canada

Learn how to set up Profit First accounts for Canadian businesses. A practical guide to account structure, naming, transfers, and cash management.

Ahmed Shafik

Co-founder

Trusted by 15,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

Setting money aside is one thing. Organizing it so you can actually stick to your Profit First® plan is another. The account structure is what turns Profit First® from a concept into something you can run every day without guesswork.

This guide walks through how Profit First® accounts work, how many you need, how to name them, and how Canadian businesses can map the structure inside a platform like Venn. If you want a high-level overview of the method itself, check out our Profit First® Method guide.

Once you understand the method, the next step is simple: build the financial setup that makes it work.

The Profit First method was created by Mike Michalowicz and introduced in his book Profit First. Profit First® is a registered trademark of Mike Michalowicz.

What are Profit First accounts?

Profit First accounts are separate buckets inside your financial platform that each serve a specific purpose. When revenue arrives, you distribute it across these buckets based on your percentages and use each account only for its intended function.

Think of these accounts as containers that create clarity:

- One for profit

- One for owner’s compensation

- One for taxes

- One for operating expenses

- Optional buckets for payroll, debt reduction, or reserves

The goal is not to complicate your finances. It is to give every dollar a job. When profit, tax, and owner’s pay have their own homes, you stop making decisions from a blended balance that hides your real spending power.

How many Profit First accounts do you actually need?

The original framework recommends five core accounts, but Canadian businesses often add one or two more to handle GST/HST, payroll, or multi-currency flows. In practice, most small businesses operate well with:

1. Income account

All revenue lands here. You do not spend from this account. You only use it to distribute funds into the buckets below.

2. Profit account

This is your buffer and reward for running the business. Funds accumulate here quietly until quarterly distributions.

3. Owner’s compensation account

This covers your salary or dividends. Treating owner pay as a fixed allocation keeps compensation predictable instead of reactive.

4. Tax account

Canadian businesses must set aside enough for corporate tax and, if registered, GST/HST. Keeping these funds separate prevents accidental spending.

5. Operating expenses (OpEx) account

This is the account you operate the business from. All vendor payments, subscriptions, transfers, and team cards draw from here.

6. Optional: Payroll account

If you run payroll, isolating payroll funds helps ensure employees are always paid on time.

7. Optional: Debt reduction or reserves account

This account is for debt repayments or future investments so they do not compete with daily operations.

You do not need all of these on day one. You can start small and add buckets as the system becomes part of your routine.

How to name your Profit First accounts

Use names that match your internal language. The important part is that the label removes ambiguity. You should never open an account and wonder what it is for.

When accounts are labeled properly, both you and your team can see at a glance what money is available and what money is off limits. Here are some common naming patterns you can use:

How Profit First accounts work in practice

Once the accounts exist, the system becomes a simple rhythm.

Revenue arrives in your Income account. On your allocation days (often twice per month), you:

- Check the balance of the Income account.

- Apply your percentage allocations.

- Distribute the funds to the Profit, Owner’s Pay, Tax, OpEx, and optional buckets.

Then you operate entirely out of the OpEx account. If an expense exceeds what is in OpEx, the constraint is intentional. The solution is not to pull from Profit or Tax. It is to adjust costs, pricing, or timing.

This is how the structure enforces financial discipline without manual spreadsheets or mental math.

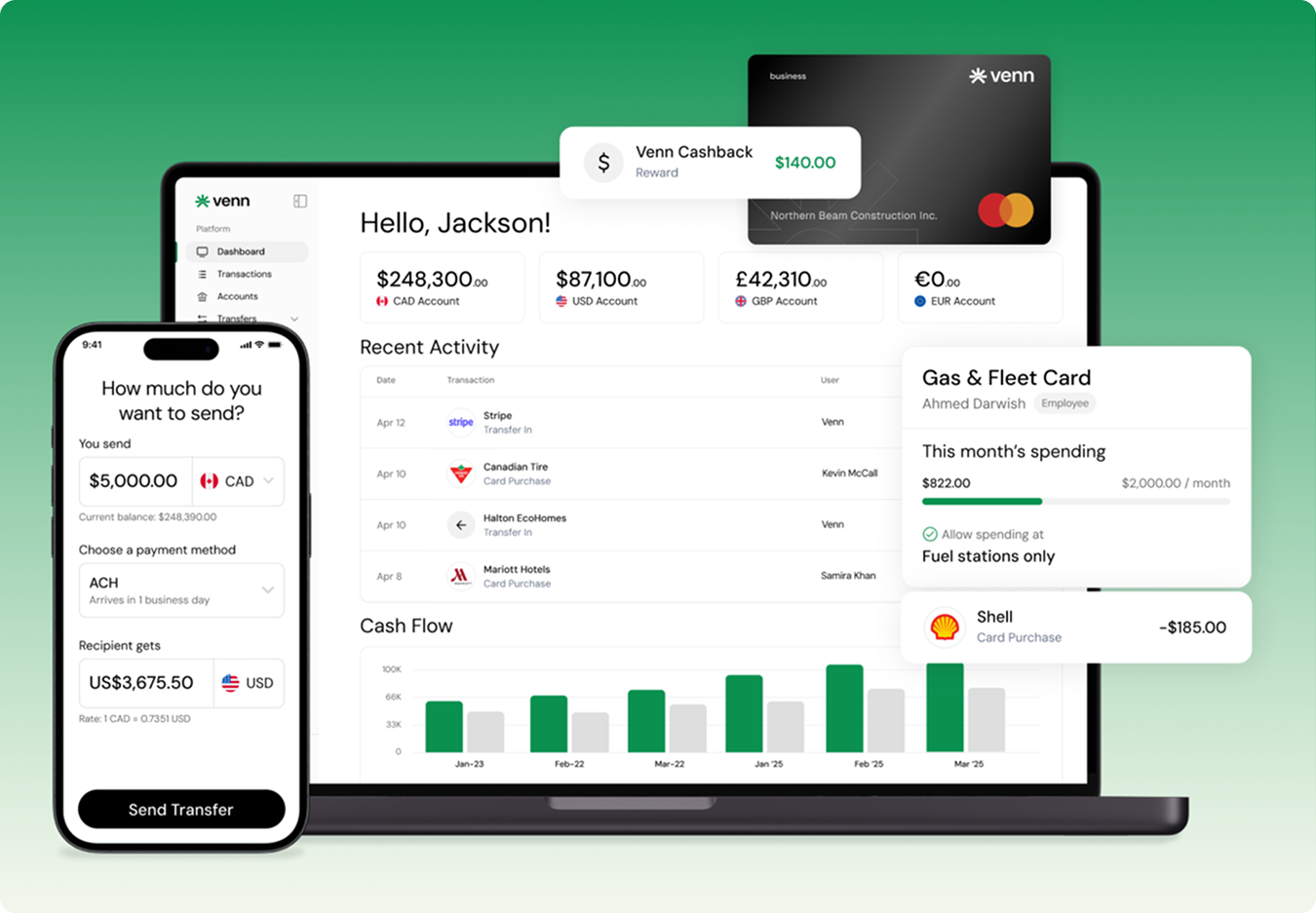

How to set up Profit First accounts inside Venn

Canadian businesses can set up a Profit First structure inside Venn in a few minutes. Venn lets you open multiple accounts and hold balances in USD, GBP, and EUR. That flexibility helps you build buckets for both domestic and international operations.

Here is how the setup typically looks inside Venn:

Income account

Your primary CAD account receives payments from customers. If you invoice in USD or EUR, you can route those payments into the appropriate currency account using Venn’s Global Accounts.

Profit, Owner’s Pay, and Tax buckets

You can open additional CAD accounts for each of these buckets. Since every account is separate, funds stay isolated and easy to track. If you invoice or pay in multiple currencies, you can also create buckets in USD, GBP, or EUR to avoid unnecessary conversions.

Operating expenses account

This account handles card payments, vendor bills, subscriptions, and transfers. You can connect corporate cards to this account to keep spending contained within your OpEx budget.

Payroll or reserves account

If payroll or planned future spending needs tight control, you can create additional accounts for those categories.

Payments and transfers

Ou Global Transfers feature lets you pay domestic vendors or international partners directly from the appropriate bucket, without mixing tax or profit funds with operating money.

How to run Profit First allocations day-to-day

The core allocation cycle stays consistent across revenue patterns.

Organized accounts make year end smoother because tax and profit funds are clearly separated all year long.

How to manage Profit First accounts if you work in multiple currencies

Many Canadian SMBs operate internationally. They invoice in USD, pay suppliers in GBP, or receive transfers in EUR. Profit First still works. The account structure simply expands to match your currency flows.

Inside Venn, businesses can:

- Hold revenue in the currency it arrives in

- Create a Profit or Tax bucket in that same currency

- Use Global Transfers to pay foreign vendors from the correct currency

- Convert only when necessary, rather than using a single CAD bucket for everything

This prevents FX costs from distorting your Profit or Tax allocations.

Common mistakes when setting up Profit First accounts

1. Too many buckets too quickly

Start simple. Grow the structure as you get comfortable.

2. Using the OpEx account as a catch-all

Every account has a purpose. Pulling from Profit or Tax destroys the system.

3. Converting foreign currency prematurely

Hold USD, GBP, or EUR in their own buckets until you intentionally choose to convert.

4. Not reviewing bucket targets quarterly

Allocations must evolve as your margins, headcount, or revenue change.

5. Mixing personal and business accounts

Profit First only works when all accounts are business accounts. Keep owner compensation and distributions clean and separate.

Is a Profit First account structure right for your business?

A Profit First account setup is most useful for Canadian SMBs that want clearer cash flow controls, predictable tax funding, and less guesswork in daily financial decisions. When each dollar has a defined account and purpose, spending becomes intentional instead of reactive.

If you want to build a Profit First system that works in practice, Venn gives you the infrastructure to do it. Try it out today!

Frequently Asked Questions (FAQ)

Q: Can I run Profit First if I use accounting software like QuickBooks or Xero?

A: Yes. Profit First operates at the cash-flow level, not inside your general ledger. Your accountant can map your Profit First accounts to your chart of accounts so reconciliations stay clean. Most owners simply tag each bank account to the appropriate category in their software.

Q: Can I automate Profit First transfers?

A: Automation is optional. Some Canadian businesses prefer manual transfers to stay closely aware of cash flow. Others use scheduled transfers within their financial platform to move funds on allocation days. Both methods work as long as allocations remain consistent.

Q: How do I transition into Profit First if I already have one blended operating account?

A: Most businesses start by opening new accounts and routing all future deposits into the Income account. Existing balances can be transitioned gradually—there’s no requirement to move all historical funds on day one. A phased transition helps avoid cash flow disruption.

Q: Does Profit First work if I use multiple payment processors?

A: Yes. Whether deposits come from Stripe, Shopify, Interac, PayPal, or wire transfers, everything should flow into your Income account first. Centralizing deposits is the key so allocations happen from a single source rather than money being scattered across different inflow accounts.

Q: Do I need a separate payroll system if I create a Payroll account?

A: No. The Payroll account simply helps ensure cash is set aside ahead of each pay cycle. You can continue using your current payroll software or provider—the account just strengthens funding discipline.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Profit First® is a registered trademark of Mike Michalowicz, who created the method and detailed it in his book Profit First. Venn is not affiliated with or endorsed by Mike Michalowicz or the Profit First brand; this article is an independent guide to applying the method.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 15,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 15,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.