CDIC Protection and Venn: What It Means For Your Business

Understand how CDIC protection applies to funds held through Venn trust accounts, coverage limits, and what to do if your balance exceeds $100K.

Ahmed Shafik

Co-founder

Trusted by 10,000+ Canadian businesses

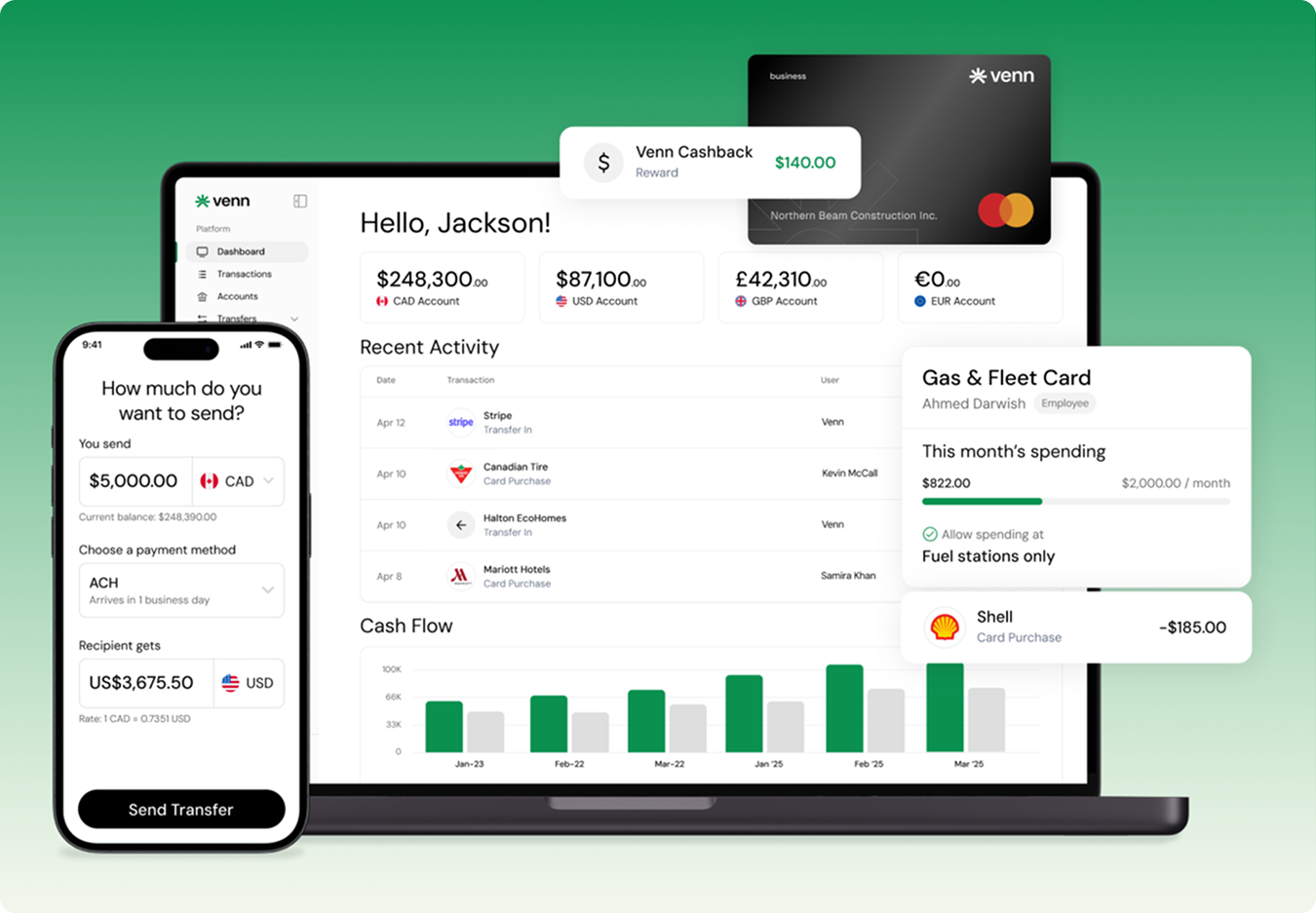

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

If you’re a Canadian founder or finance lead, you probably care about two things when you pick a financial platform:

- Can I run day-to-day money movement without friction?

- If something goes wrong, what happens to the balance I’m holding?

This post focuses on #2: CDIC protection and what it means when your Venn balance is held in trust accounts at a CDIC member institution.

We updated our Terms of Service effective September 10, 2025, to reflect how customer funds are safeguarded and how CDIC coverage limits may apply. Let's unpack what that means for your business.

Key CDIC Insurance Terms Every Canadian Business Should Understand

People often reduce CDIC protection to a single line: “Your money is insured up to $100,000.” That shortcut misses what actually matters.

How your funds are protected depends on a few specific concepts that work together. If you remember nothing else from this article, remember these four terms. They decide when protection applies, how much is covered, and who the coverage belongs to.

1. CDIC Protection

CDIC protection is the federal deposit insurance framework that applies to eligible deposits held at a CDIC member institution. It is automatic and free, but it is not universal. Protection only applies when funds meet CDIC’s eligibility rules, including where the money is held and how it is recorded. This is why the underlying account structure matters more than the brand or interface you use to access it.

2. CDIC Coverage Limit

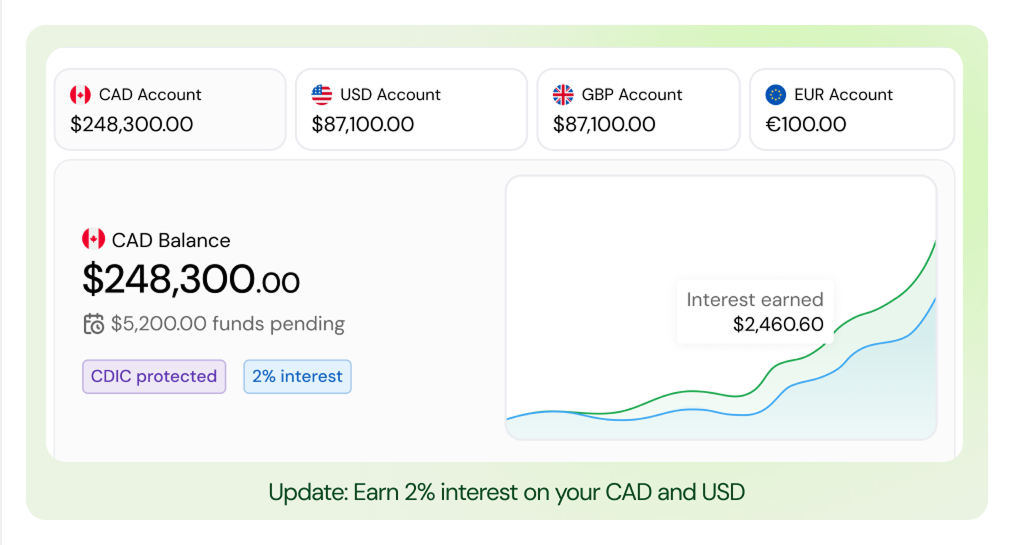

CDIC does not insure “everything in one bucket.” Instead, it protects eligible deposits up to $100,000 CAD per deposit category, per CDIC member institution, per beneficiary, as long as CDIC’s requirements are met. This distinction matters for businesses that hold larger operating balances, multiple accounts, or funds on behalf of clients. Understanding the limit helps you decide how much to keep in a single structure and when to move excess funds elsewhere.

3. Trust Accounts

A trust account is an account where funds are held by a trustee for the benefit of someone else. In this case, Venn holds customer funds in designated trust accounts at a CDIC member institution. Trust accounts can be eligible for CDIC protection, but only when specific disclosure and record-keeping requirements are satisfied. This is especially relevant for businesses that hold money temporarily, manage funds on behalf of clients, or need clear legal separation between operating funds and third-party funds.

4. Beneficial Owner

The beneficial owner is the person or business that ultimately owns the funds, even if those funds are held in trust by another party. For Venn customers, this means your business is recorded as the beneficial owner of the balance held in trust. CDIC uses beneficial ownership to determine who is entitled to coverage and how limits are applied. Without clear beneficial ownership records, coverage may not apply as expected.

Together, these four concepts explain why CDIC protection isn’t just about where your money sits, but how it is structured and documented.

How Venn Holds And Safeguards Your Business Funds

Venn safeguards customer funds by holding them in designated professional trustee trust accounts at Bank of Montreal, a Canada Deposit Insurance Corporation (CDIC) member institution.

Venn is a technology company and not a bank or a financial institution, and Venn account balances are not deposits. CDIC eligibility applies only to funds held in the trust accounts at the CDIC member institution, subject to CDIC’s requirements. These funds are legally segregated from Venn’s own operating assets and recorded to you as the beneficial owner. That separation means your balance does not sit on Venn’s balance sheet and is not exposed to Venn’s business risks.

Because the funds are held in trust at a CDIC member institution, eligible deposits may qualify for CDIC protection at the member institution level, provided CDIC’s requirements are met.

That final condition is important. CDIC protection isn’t a label or a feature you toggle on. It’s a legal framework that depends on how funds are structured, how ownership is recorded, and whether CDIC’s disclosure and record-keeping rules are satisfied at the member institution. This is why the underlying trust structure, not just the platform interface, determines how protection applies.This follows the way CDIC generally treats eligible trust-held deposits, subject to its disclosure and record-keeping requirements.

What CDIC does (and does not) cover

CDIC is a federal Crown corporation that protects eligible deposits if a CDIC member institution fails. The key word is eligible. Coverage depends on the type of balance, how it’s held, and whether the required records and disclosures are in place at the member institution.

Venn’s Terms of Service outline how customer funds are safeguarded in trust and how eligibility is determined under this structure.

CDIC generally does not cover:

- Losses due to fraud or theft (this is a separate risk category)

- Investment products like mutual funds, stocks, or ETFs

We'll focus on business operating balances held through Venn’s trust structure, where CDIC eligibility may apply when requirements are met. For a detailed background on what is CDIC Insurance, check out our guide here.

Where the $100,000 limit comes from (and how it applies)

You’ll often hear “CDIC covers up to $100,000.” The more accurate version is:

CDIC protects eligible deposits up to $100,000 per deposit category per CDIC member institution, per beneficiary, provided CDIC’s disclosure requirements are met.

For businesses, the two most relevant concepts are:

1) Deposit categories exist

CDIC coverage is calculated by category at each member institution. Trust deposits are treated differently than “in one name” deposits, and CDIC’s rules describe how those categories work.

2) Trust deposits have disclosure requirements

To receive separate CDIC protection for deposits held in trust, CDIC requires that the member institution’s records reflect that the balance is held in trust and include specific information about trustees and beneficiaries.

This matters because it affects whether CDIC protection applies as expected in a failure scenario.

How Does CDIC Protection Apply To Your Venn Balance?

Here’s the clear way to think about it.

When your funds are held as safeguarded balances in Venn’s trust accounts at a CDIC member institution, they sit within the CDIC framework that applies to trust deposits. That means those balances are structured to be eligible for CDIC protection, subject to CDIC’s standard rules. The details matter not because coverage is uncertain, but because CDIC protection is always assessed based on structure, records, and timing, not branding.

From there, two practical implications matter for how you operate day to day:

Eligible when funds are in trust accounts

Venn’s Terms describe “Safeguarded Funds” held in trust under Canadian laws/regulations, separate from Venn’s corporate funds, and not made available to Venn’s creditors. That’s the legal segregation piece that finance teams care about.

Not eligible when funds are “in-transit”

Venn’s Terms also describe a window where inbound funds can be “In-Transit” until they clear, settle, and are transferred into a trust account (the excerpt mentions it can take up to five business days). During that time, those funds are not safeguarded funds and are not held in a trust account.

If you’re managing tight cash flow around payroll or tax remittances, that timing nuance is worth understanding operationally.

What this means in real business scenarios

Here are common “Canadian SMB reality” scenarios and how to think about them.

Scenario A: You keep $40,000–$80,000 as an operating buffer

If your operating buffer is under the CDIC coverage limit (and the funds are held in the trust structure at the CDIC member institution with requirements met), you’re generally aligning with the intent of CDIC protection: reducing tail risk from a member institution failure.

What to do next:

Confirm your team understands the difference between available balance vs in-transit timing around big inbound payments.

Scenario B: You regularly hold more than $100,000

If your balance can exceed $100,000, you’re now in “coverage strategy” territory.

CDIC protection is not a blanket statement of “everything is protected.” It’s calculated within limits and categories.

What to do next (practical controls):

- Decide on a target “platform operating cap” (for example, a payroll + AP buffer).

- Move excess balances to your treasury strategy (often a separate institution or instrument), based on your risk tolerance and cash needs.

- For businesses holding third-party funds (see Scenario D), make sure your record-keeping aligns with CDIC trust requirements.

Scenario C: You run multi-currency operations (CAD + USD + more)

Businesses using Venn often care about multi-currency workflows: receiving in core currencies and paying vendors globally.

From a protection standpoint, the key is still where the funds are held and how they’re recorded (trust accounts at a CDIC member institution, CDIC requirements met). The currency workflow is operational; the protection framework is structural.

Why this matters beyond “peace of mind”

Most founders and finance managers don’t wake up excited about deposit protection. They care because it reduces distraction and supports better operating decisions:

- Cleaner risk posture: Knowing funds are legally segregated and structured for eligibility changes how you think about platform risk.

- Better controls for audits and stakeholders: If you’re reporting to investors, lenders, or a board, this is one of those questions that comes up early.

- Operational clarity: Understanding “in-transit” timing helps you avoid self-inflicted cash crunches.

Key takeaways

- CDIC protection is about the underlying structure: eligible deposits held at a CDIC member institution, with CDIC requirements met.

- The CDIC coverage limit is generally $100,000 per deposit category per CDIC member institution per beneficiary, with trust disclosure requirements that matter in practice.

- With Venn, customer funds are held in trust accounts at a CDIC member institution and are legally segregated from Venn’s corporate funds, as described in the Terms you provided.

- Build simple operating rules for balances above $100,000, and make sure your team understands “in-transit” timing around large inflows and outflows.

Ready to simplify your tax compliance and financial operations? Get started with Venn today!

Frequently Asked Questions About CDIC Protection For Businesses (FAQ)

Q: Does CDIC protection change how I should manage daily cash flow?

A: Not really, but it should inform how much you keep as an operating buffer. Canada Deposit Insurance Corporation protection is designed to reduce tail risk, not to replace treasury strategy. Most businesses use Venn for payroll, payables, and short-term operating funds, not for parking long-term excess cash. If your balance regularly exceeds CDIC limits, that’s a signal to reassess how much you keep in your operating account versus elsewhere.

Q: What happens to my funds if Venn itself were to stop operating?

A: Funds held as safeguarded balances in trust are legally segregated from Venn’s corporate assets. They are not available to Venn’s creditors and remain held for the benefit of customers, subject to the trust structure and applicable law.

Q: Are interest-earning balances treated differently for CDIC purposes?

A: No. CDIC eligibility is based on the deposit structure and records at the CDIC member institution, not on whether interest is paid. Interest may be calculated or offered separately under Venn’s terms, but it does not change how CDIC eligibility is assessed.

Q: Is CDIC protection relevant if a failure is extremely unlikely?

A: Yes. CDIC protection is about risk design, not probability. Canada’s financial system is stable, but strong financial operations assume low-probability risks exist. CDIC provides a regulated path to recover eligible insured deposits, within applicable limits, as part of building a resilient finance stack.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 10,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 10,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.