Best Canadian Business Accounts for Global Payments in 2026

Discover the best Canadian business accounts for global payments in 2026. Compare banks and fintechs like Venn for FX rates, fees, and multi-currency features.

Trusted by 15,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

For Canadian businesses that work across borders, whether paying overseas vendors, managing remote contractors, or selling internationally, having the right business account is more than just convenience. It’s a critical tool for reducing costs, improving speed, and maintaining strong business relationships.

Many business owners still rely on traditional accounts that weren’t built for global payments. As a result, they face frustrating delays, limited currency support, and hidden fees that quietly add up. Sending a single international payment can cost upwards of 50 CAD in transfer fees alone. Add in the often-overlooked exchange rate markup, typically 2–3% above the market rate, and the total cost becomes much higher than expected.

Worse, these transfers can take days to arrive. That’s a problem when you’re trying to pay overseas contractors on time or need to settle supplier invoices quickly to keep operations running smoothly. Waiting three to five business days for a payment to clear can disrupt cash flow and strain relationships.

We’ll compare the traditional banks in Canada with Venn, an alternative fintech that more and more businesses are switching to for their global payments.

What to Look for in a Business Account for Cross-Border Payments?

When evaluating the best business account for global payments in Canada, here are the key features to consider, and why they matter:

| Feature | Why It Matters |

|---|---|

| Outgoing wire transfer fees | High flat fees, often $30–$80 per transfer, can quickly add up if you’re paying multiple vendors each month. Look for transparent or low-cost options. |

| Exchange rate markup | Many banks charge a hidden 2–3% FX margin above the market rate. That can cost hundreds, or thousands, on large transfers. Transparent FX pricing saves money. |

| Settlement speed | Traditional international wires can take 3–5 days. Modern platforms use local rails like ACH, enabling next-day or even same-day delivery. |

| Multi-currency support | The ability to hold and send funds in currencies like USD, EUR, and GBP helps avoid repeated conversions and protects margins. |

| Local banking details | Real U.S. account details (like routing and account numbers) make it easier to receive payments from U.S. clients without triggering wire fees or delays. |

| Batch and automated payments | Bulk pay features simplify payroll, vendor payments, and international contractor transfers—saving time and reducing manual errors. |

| Accounting integration | Syncing directly with QuickBooks, Xero, or similar tools makes reconciling cross-border transactions easier and faster. |

What are the best options available for Canadian businesses?

When evaluating the best business account for global payments in Canada, it's critical to go beyond headline fees. The true cost of cross-border business banking includes wire fees, currency exchange markups, processing delays, and multi-currency capabilities. Below is a side-by-side comparison of leading providers in Canada, including major banks and fintech options like Venn, the preferred solution for Canadian businesses that prioritize cost-efficiency, speed, and transparency when making international payments.

| Provider | Outgoing Wire Fee | FX Markup | Settlement Speed | Multi-Currency Support | Local Banking Details | Batch Payments |

|---|---|---|---|---|---|---|

| Venn | Free or low flat fee | Low, transparent rates | 1–2 business days | USD, EUR, GBP, and more | Yes – real US ACH access | Yes |

| Wise Business | From 0.48% + fixed fee | Mid-market rate | 1–3 business days | 40+ currencies | Yes | Yes |

| RBC | $15–$45 | Undisclosed | 2–5 business days | USD and others | Partial | Yes |

| TD | $50 | Undisclosed | 2–5 business days | USD | No | Yes |

| CIBC | $30–$80 | Not disclosed | 1–3 business days | USD | Limited | Yes |

| BMO | $50 | Unpublished markup | 1–2 business days (Global Pay) | USD and others | Partial | Yes |

Venn Business Account for Global Payments

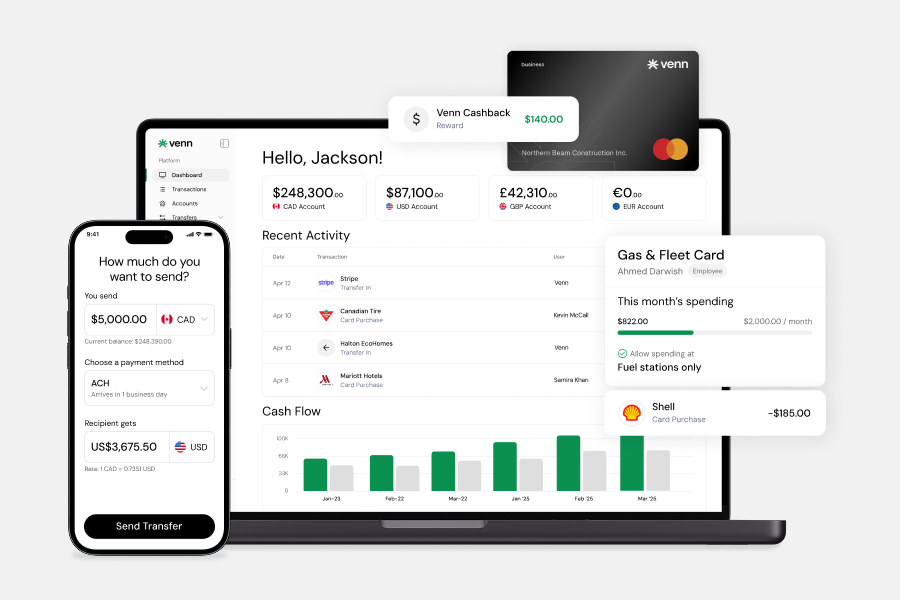

Venn is quickly becoming the go-to business account for Canadian companies making cross-border payments. Built specifically to address the pain points of traditional banking, high fees, slow settlement times, and limited currency support, Venn delivers a streamlined experience tailored for global commerce. Whether you're paying overseas vendors, managing payroll for remote teams, or receiving payments from U.S. clients, Venn offers real-time visibility, lower costs, and faster delivery. From the mobile app, businesses can access available funds, send payments, and create cards directly from their phone.

Key features:

- Cheapest International Payment Options: $6 CAD international wires, $0 ECH/ACH payments, Free unlimited e-transfers

- No fee on receiving wires: Unlike other vendors, Venn does not charge a fee on receiving money into your account

- Interest on Balances: Venn offers 2% interest on all CAD/USD balances. No minimums or lock-in periods.

- Market-Leading FX Rates: Venn offers ultra-competitive exchange rates with no hidden markup, saving businesses up to 3% compared to traditional banks.

- Same-Day Payments: Most international payments settle within one business day, with U.S. ACH payments often arriving same-day.

- Real USD Banking Details: Businesses get U.S.-based routing and account numbers to receive ACH payments like a local, ideal for clients or platforms like Stripe, Amazon, and Shopify.

- Multi-Currency Support: Hold, convert, and pay in multiple currencies, including USD, EUR, GBP, and more, all from a single interface.

- Automated Workflows: Batch payments, scheduled transfers, and CSV uploads make managing international vendor and contractor payments fast and error-free.

- Accounting Integrations: Seamlessly connect to platforms like QuickBooks and Xero to automate reconciliation and reduce month-end workload.

- No Monthly Fees: Unlike most banks, Venn doesn’t charge recurring account or maintenance fees.

Pros and Cons

| Pros | Cons |

|---|---|

| Cheapest international payment options — $6 CAD wires, $0 ACH, unlimited free e-transfers | Requires digital onboarding (no in-branch setup) |

| No fee on receiving wires — unlike most Canadian banks | Limited cash deposit functionality |

| Same-day ACH payments to the U.S. | No access to loans or credit lines |

| Best FX rates in Canada — no hidden markup | |

| Holds and sends in multiple currencies | |

| Real U.S. account and routing numbers |

Wise Business

Wise is a fintech-first solution for cross-border payments and multi-currency accounts. Many Canadian businesses adopt it when traditional banks become too costly or opaque for international operations.

Overview

Wise emphasizes transparent FX pricing, multi-currency capabilities, and local account details in several jurisdictions. It’s often used as a complement or alternative to bank accounts when businesses need flexibility in handling global payments without opaque markups.

Key Features

- Supports sending from 31+ currencies, converting to 50+ currencies.

- Uses mid-market exchange rate with low, upfront fees, starting around 0.48%.

- Local account details (IBANs, routing numbers, etc.) in many currencies, letting clients receive payments “locally”

- Batch payment support / CSV uploads for supplier or contractor payments.

- Integration with accounting tools (QuickBooks, Xero) to simplify reconciliation.

- No monthly subscription required (you pay per transaction or feature).

Pros and Cons

| Pros | Cons |

|---|---|

| Transparent FX vs. bank markups | Incoming wire reception fees (~$6.11 USD) |

| Broad multi-currency support | Speed can vary by corridor |

| Local banking details in key markets | Doesn’t replace full-service business banking |

| Batch payments & accounting integrations | May lack support for niche currencies or workflows |

RBC (Royal Bank of Canada)

RBC is one of Canada’s largest banks, with established global and cross-border banking capabilities, especially for USD and U.S. trade flows.

Overview

RBC offers business clients U.S. dollar business deposit accounts in Canada, cross-border transfers, and international wire services. It’s a more “traditional” option with strong trust, branch access, and financial services beyond just payments.

Key Features

- U.S. dollar business deposit accounts allow you to hold USD without conversion at every transaction.

- Cross‑border transfers (between Canadian and U.S. RBC accounts) can happen with no wire fee

- Online and branch‑based support, ability to deposit U.S. checks, use ACH origination for U.S. vendors.

- RBC’s “International Business Banking” offering supports payments in various currencies and more efficient cross-border flows.

- Scale into other currencies by converting (though FX margins are not always transparent).

Pros and Cons

| Pros | Cons |

|---|---|

| Strong brand trust and banking stability | FX markups not publicly disclosed |

| Support for cross-border USD operations | Slower settlement for non-USD corridors |

| Integrated lending and credit services | Limited transparency on total transfer costs |

TD (Toronto-Dominion Bank)

TD offers cross-border banking services and a “Global Transfer” product for moving money internationally.

Overview

TD positions itself as a bridge for clients operating between Canada and the U.S., offering cross-border account linking, U.S. dollar accounts, and international payment tools. It’s most competitive for businesses with heavy U.S. exposure.

Key Features

- Cross-Border Banking: integrated access to Canadian and U.S. accounts, allowing clients to manage both through one interface.

- TD Global Transfer: tools to send money via Visa Direct or International Bank Transfer depending on the corridor.

- Conversion between Canadian and U.S. dollar accounts directly.

- Support for multi-currency transfers in many common currencies.

Pros and Cons

| Pros | Cons |

|---|---|

| Reliable for Canada–U.S. cross-border flows | FX margins not clearly disclosed |

| Convenient account linking between regions | Fallback to wire may incur higher fees |

| Trusted bank infrastructure and support | Not optimized for multi-currency vendor payments |

CIBC (Canadian Imperial Bank of Commerce)

CIBC offers a specialized international payment product for business clients, called CIBC Global Money Transfer (GMT).

Overview

CIBC’s GMT is designed to provide cost-effective outbound global payments from Canadian accounts to 130+ countries, with some favorable features versus standard bank wires.

Key Features

- Zero CAD transfer fee for many corridors (for qualifying business accounts).

- Fast delivery: many payments reach recipients in one business day.

- High transfer limits (e.g. up to 100,000 CAD per transaction).

- Ability to send in local currency or USD (where eligible).

Pros and Cons

| Pros | Cons |

|---|---|

| No-fee transfers in many corridors | FX spread not fully transparent |

| Fast settlement for many currencies | Fallback to wires for unsupported routes |

| High per-transaction limits | Limited automation for high-volume businesses |

BMO (Bank of Montreal)

BMO offers an integrated tool called Global Pay for international business payments, embedded in its business banking platform.

Overview

BMO Global Pay is BMO’s modernization effort for international payments. It enables smaller value cross-border transfers through a more modern rail while keeping integration with a bank’s conventional systems.

Key Features

- Payment support to 30+ destinations built into BMO’s online banking for business.

- Payment limits up to CAD 100,000 for eligible currencies.

- Transparent exchange rate shown before you send.

- Faster settlement: many payments arrive in 1–2 business days; some even in minutes.

- No extra setup: uses existing wire infrastructure.

Pros and Cons

| Pros | Cons |

|---|---|

| Integrated directly into BMO online banking | Limited country and currency coverage |

| Fast settlement in supported corridors | FX rates include markup, not mid-market |

| Streamlined for BMO business clients | No advanced vendor payment automation |

Understanding the Hidden Costs of International Payments

When evaluating global payment providers, most business owners focus on the visible numbers, the wire fees or monthly account charges. But those figures often disguise the true cost of international money movement. The real expenses are often buried in less-transparent elements like foreign exchange markups, bundled fee structures, and inefficient currency conversion workflows.

FX Markups: The Silent Margin

Many banks and traditional providers advertise “low fees” but quietly add a spread of 2%–3% on top of the mid-market exchange rate. For a $20,000 USD vendor payment, that adds up to $400–$600 CAD in hidden costs, significantly more than the flat transfer fee.

In contrast, modern fintechs like Venn offer you the real exchange rates, with a clearly stated conversion fee. This not only reduces total costs but also builds trust with vendors who receive more on their end.

Bundled Fees in the Exchange Rate

The term “no wire fee” can be misleading. In many cases, the fee is simply embedded within a less-favorable FX rate. While it may look like you’re saving on transaction fees, your supplier ends up receiving less, and you, unknowingly, pay more.

Currency Conversion Without Control

If your business receives foreign currency into a CAD-only account, your bank may automatically convert funds at its own rate, often without notice or the ability to control the timing. That’s another potential source of lost value, especially for businesses that could benefit from holding multiple currencies.

How to Spot the Real Cost

To get a full picture of your payment provider’s pricing:

- Compare their exchange rate to the real mid-market rate on platforms like Google or Reuters.

- Ask for the all-in cost, including FX markups and wire fees.

- Look at how currency conversion is handled for incoming payments.

- Prioritize transparency and multi-currency control, not just headline fees.

This section helps anchor the value of using purpose-built tools like Venn, which eliminate many of these hidden costs through mid-market FX rates, transparent pricing, and more control over currency conversion timing.

Which Business Account Is Best for Global Payments?

Ultimately, the best global payment account depends on your business priorities. If you're looking for legacy banking relationships, in-person service, or bundled products like loans and payroll, the Big Five Canadian banks still have a place, even if it comes at a premium.

But if your priority is lowering costs, speeding up payments, and managing multiple currencies with ease, Venn is the clear leader. With competitive FX rates, no hidden fees, and tools designed specifically for modern Canadian businesses, Venn is trusted by growing companies to handle international vendor payments with confidence and clarity.

Whether you're paying a contractor in Germany, importing goods from China, or managing a remote team in the U.S., Venn gives you a faster, cheaper, and smarter way to make global payments.

Frequently Asked Questions (FAQ)

Q: What’s the best way to pay international vendors from Canada?

The most cost-effective way is to use a modern fintech provider like Venn that utilizes local payment rails (ACH, SEPA) and offers transparent, low exchange rates. This approach avoids the high wire fees ($30-50) and hidden FX markups ($2-5%$) typically charged by traditional Canadian banks.

Q: How much does it cost to send money internationally from a business account?

The cost varies significantly. Traditional banks charge wire fees between $30–$80 per wire, plus a hidden FX markup that can add an extra 2–3% to the total amount. Modern platforms like Venn charge a much smaller, transparent fee and use a real exchange rate (often a margin as low as 0.25%), which can save businesses thousands annually.

Q: Can I hold foreign currencies in a Canadian business account?

With most traditional banks, you are limited to holding only USD. Digital platforms like Venn offer multi-currency accounts that let you hold, convert, and send in over 30 major currencies (including CAD, USD, GBP, and EUR). This allows you to manage conversions strategically and avoid being "double-converted" every time you pay an overseas vendor.

Q: How fast do global business payments arrive?

Payments sent via the traditional SWIFT network through a bank can take 3–5 business days. However, transfers sent using local payment rails through a platform like Venn often arrive much faster, typically within 1–2 business days, and sometimes even same-day, depending on the destination and currency.

Q: Is it safe to use a fintech like Venn for international business payments?

Yes. Venn is a secure and regulated platform designed for Canadian businesses. It is registered with FINTRAC and is a registered Payment Service Provider (PSP) under the Bank of Canada. Furthermore, Venn partners with federally regulated institutions, meaning eligible funds are covered up to $100,000 under CDIC insurance.

The comparative information provided on this page is based on publicly available sources and is accurate to the best of our knowledge as of September 20, 2025. Features, pricing, and terms may change without notice. For the latest information, please consult each provider’s official website directly. All trademarks and product names are the property of their respective owners. Their use does not imply any affiliation with or endorsement by those brands.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 15,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 15,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.