How to Choose the Best Business Credit Card for Construction Companies in Canada

Discover the best business credit card for Canadian construction companies. Compare features, rewards, and tools built for contractors, crews, and job sites.

Ahmed Shafik

Co-founder

Trusted by 15,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

Running a construction business in Canada means dealing with unpredictable timelines, high upfront costs, and uneven payment cycles. Materials and equipment often need to be purchased weeks before any revenue is collected. Meanwhile, expenses like fuel, permits, rentals, and subcontractor payments can’t wait.

This mismatch between when you spend and when you get paid puts strain on working capital and makes it difficult to manage operations across multiple job sites. It’s not just about paying bills, it’s about keeping projects on track, crews equipped, and suppliers satisfied. 91% of construction managers indicated that they were involved in a project that experienced delays in the last 3 years, with the majority listing resourcing issues and planning as the primary reasons for these delays. A corporate card helps to manage spend across job sites and gives you and your finance team the insight you need into your team's spend.

Whether you run a small general contracting business or manage several teams across provinces, having the right financial tools in place can make a measurable difference.

Why a Standard Business or Personal Credit Card Isn’t Enough

Many contractors default to using personal cards or standard small business credit cards from big banks. Others rely on Amex, only to discover it is not accepted by key suppliers or trades.

These options might work in the short term, but over time they introduce challenges:

- Business and personal spend gets mixed, creating tax-season headaches

- You have limited visibility into project-level spending

- Reimbursement processes for field purchases become manual and inconsistent

- FX fees and wire costs add up when dealing with cross-border vendors

- Most cards offer little in the way of employee controls or job-site accountability

Construction isn’t a typical business, and generic cards aren’t built for how contractors spend. Between equipment rentals, fuel runs, materials orders, and field-based purchasing, the right solution needs to support real job-site workflows while helping you keep control of your cash flow.

Why Project-Based Categorization Matters for Construction Spend

Field worker spending is unpredictable but essential.

Construction crews often make same-day purchases to keep work moving, whether it’s a run to Home Depot for a specific fitting, buying fuel for skid steers, or picking up lunch during a 14-hour shift. These expenses, while small individually, add up quickly and must be linked to the correct job code. If left uncategorized, they can erode project margins and delay cost reconciliation.

Project-specific tracking is not optional, it’s foundational.

Unlike other industries that rely on monthly close cycles, construction companies operate on a job-costing model. That means every dollar spent must tie back to a site, a client, or a phase of a build. Materials alone can account for up to 80% of total project costs, and labour adds another 20–35%. Without project-based tracking, companies risk underbilling, overpaying, and misquoting future jobs.

What that looks like in practice:

- A site supervisor needs a virtual card to order $4,000 in drywall for a condo project before noon.

- A foreman fills two trucks with diesel en route to a northern build site and texts in the receipt on the go.

- A project manager uploads a $3,200 permit payment to the municipal office using a Venn corporate card tied to a school renovation project.

When spend is tracked this way, you get a real-time understanding of profitability by project, not just end-of-month guesses. And when integrated with tools like QuickBooks or Xero, those entries sync automatically, reducing admin time and avoiding costly manual errors.

What to Look For in a Corporate Card Built for Construction?

| Feature | Why It Matters for Construction Companies |

|---|---|

| Cash Back & Rewards | Offset high-volume expenses like gas, materials, and tool rentals. For firms with predictable category spend, this can generate thousands in annual value. |

| Project-Based Spend Tools | Track purchases by job site or project code to simplify billing, improve job costing accuracy, and avoid budget overruns. |

| Virtual & Employee Cards | Allow PMs or crew leads to make necessary purchases without sharing physical cards. Helps control job-level expenses while enabling fast purchases in the field. |

| Spend Controls & Limits | Set daily or category limits by employee or job, reducing over-spend risk and simplifying internal approvals. |

| 0% Intro APR Options | Useful for managing large upfront material or equipment costs before client payments are received. Helps manage seasonal cash flow constraints. |

| No Annual Fee | Ideal for small to mid-sized construction businesses with moderate spend or limited use of travel perks. |

| Low FX or Cross-Border Fees | Helpful for companies buying from US suppliers or paying subcontractors across the border. |

| Accounting Software Integration | Syncs with tools like QuickBooks or Xero, reducing manual entry and ensuring clean records tied to project budgets. |

| Receipt & Job Code Capture | Speeds up month-end close and keeps finance from chasing field receipts. Crucial for T&M or cost-plus projects where backup is needed for client invoicing. |

How These Features Support Canadian Construction Businesses

Cash Back & Rewards

Construction companies often rack up tens of thousands in monthly spend on gas, lumber, cement, tools, and subcontracted services. A business card that rewards these categories, especially if cash back is uncapped or automatically applied, can turn routine purchases into real returns. Even a 1% return on $30,000 monthly spend equals $3,600 annually that can go back into your business.

Project-Based Spend Tools

Job costing is non-negotiable in construction. Tools that tag each transaction with a project code or client name help avoid underbilling, reduce reconciliation time, and make audits cleaner. Without this, shared cards or vague expense categories can eat into your margins or delay client billing.

Virtual & Employee Cards

Whether it’s a foreman placing a last-minute order or a project manager needing to secure crane rentals, having access to virtual or employee-issued cards means you don’t need to run every purchase through head office. This speeds up procurement while keeping spending under control, especially useful on remote or concurrent job sites.

Spend Controls & Limits

Not every team member should have the same purchasing power. Modern business cards let you set daily, category-based, or project-specific spend limits. That means a site lead can buy $500 of safety gear but not a $2,000 generator without approval. This reduces misspend and makes your finance team’s job easier.

0% Intro APR Options

Many Canadian contractors face delays between issuing invoices and receiving payments. A card that offers a 0% interest period, often for 12–18 months, can smooth cash flow by covering upfront expenses like drywall or foundation pours before revenue lands. Just be sure to time your repayment strategy accordingly.

No Annual Fee

If you’re not a high spender or frequent traveller, skip premium perks and opt for a card with no annual fee. You’ll keep overhead lower while still benefiting from automation, spend tracking, and occasional rewards. For solo contractors or smaller firms, this can be a no-brainer.

Low FX or Cross-Border Fees

Many Canadian construction businesses import equipment or materials from the US. Without a proper multi-currency solution, you’ll pay inflated FX fees (typically 2.5–3% at major banks). Choosing a card with low or no FX markup helps you preserve margins, especially for companies working in both CAD and USD.

Accounting Software Integration

Cards that sync with accounting platforms like QuickBooks, Sage, or Xero eliminate the need for manual transaction entry. You’ll save hours at month-end and improve billing accuracy, especially when expenses are already categorized by project or vendor.

Receipt & Job Code Capture

If your site crews lose paper receipts or forget to submit expense notes, it creates admin headaches and exposes your business to compliance risk. Look for cards with mobile receipt capture, auto-categorization, and job code tagging. It turns a 20-minute chore into a 10-second text.

| Criteria | Venn Corporate Card | Big 5 Bank Business Cards | Amex (Business or Personal) | Personal Credit Cards |

|---|---|---|---|---|

| Designed for Construction Use | Yes – supports job costing, project tagging, and mobile use | No – generic categories and limited field-use tools | No – built for high-income professionals and travel | No – not intended for business or field operations |

| Multi-Currency Support | Yes – CAD, USD, GBP, EUR with smart routing | Limited – FX fees often 2.5–3% | No – high FX and limited CAD-USD support | No – high FX and not business-friendly |

| Spend Controls & Virtual Cards | Instant cards, per-project limits, full visibility | Often unavailable or limited to high-fee accounts | Available but clunky integration | Not supported |

| Project-Based Expense Tracking | Built-in job tagging, syncs to accounting tools | Manual export and reconciliation needed | Manual or third-party software required | No support |

| Approval Speed & Access | Same or next-day, no personal credit check | 5–10+ business days, often requires personal guarantee | Can require strong personal credit, long processing | Instant, but not business-optimized |

| FX Fees | 0.25% markup (or lower), no inbound wire fees | 2.5–3% plus wire fees ($15–$25 typical) | Often 2.5% or higher | Typically 2.5% or more |

| Accounting Software Integration | Seamless integration with QuickBooks, Xero, etc. | Requires CSV exports or manual mapping | May require third-party tools | Not compatible |

| Field Team Compatibility | Built for mobile receipt capture, SMS uploads | Requires manual expense entry or app logins | App-based, low construction adoption | Not usable across team |

| Builds Business Credit | Yes, under business name | Yes | Some business cards do; personal cards do not | No – builds personal credit only |

| Annual Fees | $0 | Typically $99–$150 or more | High annual fees ($250–$700) | Varies, often not worth it |

Comparing Your Options: What Canadian Construction Businesses Should Know

Venn Corporate Card

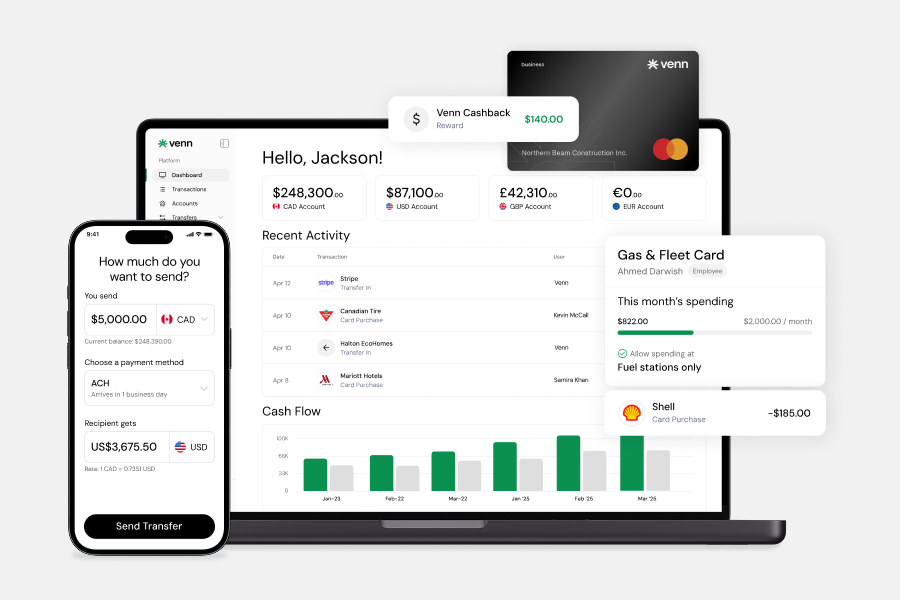

Designed for modern Canadian contractors, Venn solves real field-level problems, from job-based spend tracking to FX-free US supplier payments. It offers true CAD and USD accounts, project tagging, and mobile-friendly expense controls that field workers will actually use. From the mobile app, teams can check available funds, send transfers, and spin up new cards without waiting on the office. Venn eliminates the need for personal cards or cobbled-together tools, with no annual fee and 0.25% FX markup.

Big 5 Bank Business Credit Cards

These are familiar and widely available, but built for general small business use, not construction. Rewards are often focused on office expenses or travel, and tools like spend controls or project tagging are either missing or buried behind legacy interfaces. Getting approved can require a personal guarantee, and international payment features are often slow, expensive, or both.

American Express (Business and Personal)

Amex cards are popular among contractors for their reward programs, but come with major drawbacks. High FX fees (often 2.5%+), limited multi-currency functionality, and reward programs focused on travel make them a poor fit for Canadian construction firms that spend heavily on fuel, tools, and materials. Field teams may also struggle with merchant acceptance or submitting receipts on the go.

Personal Credit Cards

Many contractors default to using personal cards for business expenses, especially early on. But this creates issues fast: messy books, credit utilization tied to your personal file, and zero visibility into what’s being spent per job or employee. No real spend controls, no accounting integrations, and no business credit building. It might seem simpler, but it creates financial friction at scale.

How to Choose the Right Card for Your Construction Business

The right credit card can do more than cover purchases, it should match your job site needs, cash flow cycles, and team structure. Here's how to approach the decision depending on your company’s size and stage:

For Solo Contractors and Owner-Operators

If you're running a lean operation, cash flow is often your biggest constraint. You’re likely putting materials, fuel, and tools on your own card, but this limits visibility and blurs business with personal finances.

Look for:

- A card with no annual fee and reliable cashback

- Support for both CAD and USD to avoid FX fees from US suppliers

- Tools that let you tag purchases by client or job site (even if you're a one-person crew)

Avoid: Personal cards, which don’t build business credit or integrate with accounting software, and may leave you exposed at tax time.

For Small to Mid-Sized Crews

You’re managing a few job sites, subcontractors, and maybe have an office manager. You need better control over field spending without bottlenecking every Home Depot run through your own card.

Look for:

- Multi-user access with per-employee limits

- Real-time transaction visibility and mobile receipt capture

- Integration with QuickBooks or Xero for clean bookkeeping

Avoid: Big bank cards that lack real spend control features, or cards that don’t let you issue virtual cards for one-off online purchases or vendors.

For Growing Firms with Multiple Sites

Once you're managing multiple foremen, trucks, and timelines, you need a financial tool, not just a card. Visibility, control, and speed become essential.

Look for:

- Unlimited physical and virtual cards with project-specific rules

- USD/CAD accounts to streamline cross-border payments and supplier management

- Automated expense coding by job site and vendor

- Procurement features to reduce maverick spending and improve payment cycles

Avoid: Traditional cards with capped rewards or slow approval timelines. You need spend power that scales with your team and doesn’t delay operations.

Why Venn is the Best Fit for Canadian Construction Businesses

If you’re running a construction business in Canada, whether as a solo contractor or a growing firm managing crews, Venn was built with your reality in mind.

Where traditional cards fall short, Venn delivers:

- Real CAD and USD accounts for smarter payments, not “USD-like” gimmicks

- Project-based spend controls that track purchases by site, not just vendor

- 2% interest on all USD/CAD balances

- Mobile-first tools that field teams will actually use, no more lost receipts

- Fast approval, no personal credit check, and no annual fee

- Low FX fees (0.25%) to save thousands when buying from US suppliers or getting paid through platforms like Stripe or PayPal

Other cards may offer partial solutions. But only Venn brings the full financial toolkit together, so you can focus on building projects, not chasing down purchase orders, manual reconciliations, or overruns.

If you’re tired of using a personal card that wasn’t meant for this, or frustrated by big bank delays and limitations, it’s time for something purpose-built.

Venn works like your business does, fast, flexible, and built for the field.

How a Mid Sized Construction Business in Ontario Scaled Their Firm with Venn.

When a mid-sized construction firm based in Ontario, doubled their crew count and expanded to five simultaneous job sites, their finance team hit a wall.

With over 80 field employees, multiple foremen, and manual receipt tracking across job sites their legacy banking system couldn’t keep up. Tracking who bought what, for which site, and whether it was approved turned into a full-time job.

“Before Venn, we were constantly behind on job costing. Our PMs were buying materials with personal cards or calling the office for approval every time they needed something,” says their Director of Finance.

Real-Time Control Meets Field-Level Speed

Venn changed that. Within a week of onboarding, they had issued employee cards with job-specific limits to every foreman, along with virtual cards for trusted subcontractors and office staff. Every purchase was tagged to a project. Every receipt was submitted from the field the same day meaning, no more paper chasing.

“Now we know, to the dollar, what’s being spent on each job site, and we’re not waiting 30 days to figure it out”

From Reactive to Proactive Cash Flow

With Venn’s real CAD and USD accounts, the firm now pays US vendors directly by ACH, avoiding wire fees and long delays. They’ve also automated their payables with QuickBooks integration, meaning supplier invoices get paid faster, unlocking early payment discounts they couldn’t negotiate before.

“We’ve started getting 1.5% early pay discounts just by being quicker to the punch. That alone covered our monthly overhead on admin,”

The Best Business Credit Card for Construction Companies in Canada

Choosing the right credit card for your construction business isn’t just about rewards — it’s about solving real cash flow, control, and expense management challenges.

Whether you’re prioritizing high cash back on fuel and materials, managing multiple crews across sites, or trying to streamline how you pay contractors and vendors — the right business credit card should work the way your construction company does.

Venn’s corporate card is purpose-built for Canadian contractors. It offers:

- 1% unlimited cashback on every purchase — no rotating categories or caps

- Real CAD and USD cards and accounts so you can avoid FX fees on cross-border expenses

- Project-based spend controls to manage employee purchases by site or job code

- 2% interest on CAD/USD balances

- No annual fees or personal credit checks — approval based on your business

- Mobile-first expense management that actually gets used by your field teams

Unlike personal cards or general-purpose business cards from the big banks, Venn was designed to help you:

- Pay for materials, tools, and fuel when cash flow is tight

- Track every purchase by project, employee, or subcontractor

- Avoid delays and admin headaches at month-end

- Build a business credit profile without putting your personal credit on the line

If you’re looking for the best credit card for your construction business in Canada, and want a card that gives you real control, real savings, and real support, Venn is the only choice built for you.

Get the construction business credit card that works as hard as you do.

Frequently Asked Questions

Q: What is the best credit card for construction businesses in Canada?

The best card is one designed to support the operational and project-based nature of construction. This means looking for a corporate card that offers high, unlimited cashback on major expenses like fuel and materials, provides real Canadian and US dollar accounts, and includes powerful tools for job-costing and real-time expense tracking. Modern corporate cards, like those from Venn, often stand out because they offer robust spend controls and do not require a personal credit check, making them highly accessible to growing contractors.

Q: Can I use a personal credit card for my construction business?

While you technically can, it is strongly advised against. Using a personal card for business expenses complicates tax preparation, makes accurate job costing difficult, and risks commingling funds, which can expose your personal assets to business liability. A dedicated business credit card is essential because it legally separates your finances, simplifies bookkeeping, and actively builds a positive credit history for your construction company.

Q: Do construction businesses need multiple employee cards?

Yes. For businesses managing multiple crews, subcontractors, or job sites, issuing multiple employee and virtual cards is essential for maintaining control and accountability. A corporate card platform allows the business owner or project manager to issue unlimited cards with specific, site-based spending limits. This enables crews to purchase necessary gas, tools, or emergency supplies in the field while providing real-time oversight and preventing accidental overspending.

Q: How do tariffs affect construction business credit card use in Canada?

Tariffs and import duties are a major cost component when sourcing construction materials from outside Canada. A business credit card that supports native US dollar (USD) payments is crucial because it helps you minimize currency conversion markups and gives you a clear view of the true landed cost of materials, including duties. Using a dedicated USD card, like one provided by Venn, can protect your margins by reducing fees tied to cross-border purchases and delayed wire transfers.

Q: Are there business credit cards in Canada with no annual fee?

Yes, there are business credit cards available in Canada that do not charge an annual fee. While many traditional bank business cards charge annual fees, often without including the advanced expense management features needed by field teams, several digital corporate card providers, including Venn, offer no-annual-fee options. This structure is ideal for keeping overhead low while still gaining access to features like unlimited employee cards and cashback rewards.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 15,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 15,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.