Best 0% Interest Business Credit Card in Canada

Compare the best 0% interest business credit cards in Canada for 2025. Find the top low-APR options, balance transfer cards, and interest-free alternatives.

Ahmed Shafik

Co-founder

Trusted by 15,000+ Canadian businesses

Business banking for Canada

Local CAD and USD accounts, corporate cards with cashback, the lowest FX rates in Canada, free local transfers, and more.

If you're running a business in Canada, every percentage point matters, especially when it comes to managing cash flow or reducing the cost of financing. That's where 0% interest business credit cards come in.

While many Canadian business owners search for a “0% APR business credit card,” what’s actually available can be more complex. Some cards offer 0% interest only on balance transfers. Others provide short-term promotional windows. And a few, like Venn’s corporate card, operate on a completely different model, offering no interest by default because they’re structured as charge cards, not revolving credit products.

So, how do you choose the right option?

In this guide, we’ll break down the top business cards available in Canada that offer 0% APR or equivalent interest-free features. We’ll explain the fine print, compare key benefits like cashback and fees, and help you find the best card for your business needs in 2025, whether you're trying to reduce interest on a large purchase or simply optimize how your team spends.

Key Questions Answered in This Guide

- What does 0% interest mean for business credit cards?

- Are there any 0% interest business cards available in Canada today?

- Which provider gives you the best real value — not just a promo window?

What Does 0% Interest Mean for Business Credit Cards?

When a business card advertises “0% interest,” it usually refers to a promotional annual percentage rate (APR), often available for a limited time after you open the account. But there are two common types of 0% interest offers you’ll see:

1. 0% APR on Balance Transfers

This allows you to move existing debt from another card and pay it off without interest for a set period (often 6–12 months). However:

- Transfer fees usually apply (1–3% of the amount moved)

- After the promo ends, a high regular APR kicks in (usually 13–22%)

- Many of these are actually personal credit cards, not designed for business use

2. 0% APR on New Purchases

Some business credit cards offer interest-free periods for new purchases, typically for the first few months. This can help manage large upfront expenses, but:

- The 0% period is short-lived

- Interest is charged retroactively if balances aren’t paid in full

- Spending limits and terms are often tied to your personal credit profile

3. Corporate with No APR at All

Not all cards work the same. Some, like Venn’s corporate card, don’t charge interest at all, not as a limited-time promo, but by design.

These cards work on a charge card model, meaning:

- Your balance must be paid in full regularly (no interest accrues)

- You still benefit from card rewards like cashback

- You gain more visibility and control over business spending without taking on personal risk

Bottom Line:

“0% interest” may sound the same everywhere, but the terms, risks, and suitability vary widely depending on whether you’re using a personal credit product or a true business spending solution like Venn.

Are There Any 0% Interest Business Cards in Canada Right Now?

Yes, but here’s the catch: while there are several cards in Canada advertising “0% interest,” most of them are personal cards, not built for business use.

In 2025, there are three main types of cards to consider if you're looking for 0% APR:

- Promotional balance transfer cards — These offer 0% interest for a limited time on existing debt, but usually come with a transfer fee and switch to a high APR after the promo ends. Most are personal cards (like MBNA or CIBC).

- Short-term 0% on purchases — These are rarer for businesses in Canada, and the offer window is often under 3 months. You’ll also need strong personal credit to qualify.

- Corporate charge cards — Like Venn, which don’t charge interest at all because they’re not revolving credit products. There’s no teaser rate because there’s no interest to begin with. These are purpose-built for Canadian businesses.

Here’s how the top 0% interest (or interest-free equivalent) cards in Canada compare:

| Provider | Interest-Free Offer | Annual Fee | Rewards | Best For |

|---|---|---|---|---|

| Venn | Always 0% (charge model, no APR) | $0 | 1% cashback (no cap) | Canadian SMBs with global spend, accounting needs |

| American Express Business Platinum | Up to 55 interest-free days | $799 | Points, travel perks | High-spend businesses, frequent flyers |

| BMO CashBack Business Mastercard | 0% on balance transfers for 9 months (3% fee) | $0 | 0.75–1.75% cashback on select categories | Everyday local business purchases |

| CIBC Select Visa (Personal) | 0% for 10 months on balance transfers (1% fee) | $29 (rebated year 1) | Gas savings, basic perks | Sole props/startups looking to manage short-term debt |

| MBNA True Line Mastercard (Personal) | 0% for 12 months on balance transfers | $0 | None | Individuals consolidating business or personal debt |

Venn Corporate Card

Best for: Canadian SMBs that want 0% interest by default, without relying on promotional APRs or personal credit scores.

Unlike traditional business credit cards, the Venn Corporate Card doesn't charge interest, ever. That’s because Venn uses a charge card model. Your business spends using available funds, and balances are paid off regularly. No revolving credit, no compound interest, and no 12-month surprises when an introductory offer ends.

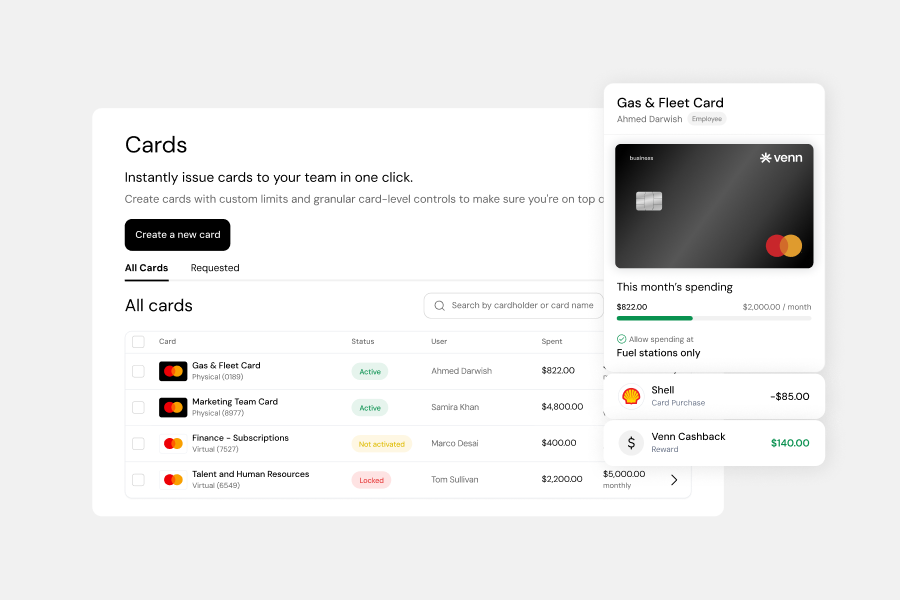

What makes Venn especially unique is that it’s purpose-built for incorporated Canadian businesses. You can issue unlimited virtual cards to your team, set custom spend limits by employee or project, and automate receipt collection and policy enforcement. From the mobile app, finance teams can access company funds, send transfers, and issue new cards right from their phone.

But the standout feature? You only need one card to spend in CAD, USD, GBP, and EUR, and Venn automatically uses the right currency balance. That means no unnecessary FX conversions or multiple cards to manage. Combined with uncapped 1% cashback on all spend, Venn delivers both flexibility and long-term savings.

You also get deep integrations with QuickBooks and Xero, real-time spend visibility, and the ability to automate payables and global transfers, all from one unified dashboard.

Key benefits:

- Always 0% interest (charge card model)

- 1% uncapped cashback on all spend

- Multi-currency support (CAD, USD, GBP, EUR) on one card

- 2% interest on all USD/CAD balances, no minimums required

- Real-time spend controls and receipt capture

- Two-way sync with QuickBooks and Xero

- Send Interac e-Transfers®, EFTs, ACH, and wires globally

- Real customer support

- No annual fees or card minimums

Note: The Venn Corporate Card is not a credit card. It does not offer revolving credit or accrue interest. Businesses must maintain a funded balance to use the card.

American Express Business Platinum Card®

Best for: High-spend businesses that want travel perks and flexibility,and don’t mind paying a premium.

The Amex Business Platinum Card doesn’t offer 0% APR in the traditional sense, but it does provide up to 55 days of interest-free spending on new purchases, making it one of the more flexible options for short-term financing. After that window, standard interest rates apply, which typically range from 20.99% to 29.99%, depending on your credit profile.

This card also differs from many traditional business cards in that it doesn’t come with a pre-set spending limit. Instead, your purchasing power adjusts based on your business profile and spending habits.

However, that flexibility comes with a price, the annual fee is $799, making it one of the most expensive cards on the list. That said, for businesses that spend heavily and frequently travel, the perks can make up for the cost. You earn Membership Rewards points, which can be redeemed for flights, hotels, gift cards, or statement credits, and you get premium benefits like airport lounge access and purchase protection.

Key benefits:

- Up to 55 days of interest-free spending

- Points-based rewards program (Membership Rewards®)

- No pre-set spending limit

- Airport lounge access and travel insurance

- Expense management tools and Amex Offers

Note: This is a true credit card. Interest charges apply if balances are not paid in full after the interest-free period.

BMO CashBack Business Mastercard

Best for: Small businesses looking for a short-term 0% balance transfer option with no annual fee.

The BMO CashBack Business Mastercard offers a promotional 0% interest rate on balance transfers for the first 9 months, making it one of the few business cards in Canada that provides a true interest-free window. However, it does come with a 3% balance transfer fee, and once the promotional period ends, purchases revert to a 20.99% APR.

The card offers tiered cashback on business spending:

- 1.75% on gas

- 1.5% on office supplies

- 0.75% on other eligible purchases

You also get purchase protection, extended warranty coverage, and the ability to issue up to 22 additional cards to employees at no extra cost.

If you’re managing short-term debt or want to consolidate balances from another card, this can be a low-friction way to ease interest costs — but it won’t be the cheapest option long-term.

Key benefits:

- 0% APR on balance transfers for 9 months (3% fee)

- Up to 1.75% cashback on business expenses

- No annual fee

- Purchase protection and extended warranty

- Up to 22 supplementary employee cards

CIBC Select Visa Card (Personal)

Best for: Sole proprietors or early-stage entrepreneurs consolidating debt — with some extra perks.

While not a true business card, the CIBC Select Visa is often used by sole proprietors and small business owners looking for 0% interest on balance transfers. The card offers a 0% APR for up to 10 months, with a 1% transfer fee.

After the promotional window, the purchase APR is 13.99%, which is lower than most mainstream credit cards. The annual fee is $29, but it’s rebated for the first year.

You also get access to CIBC’s gas discount program (up to 10 cents off per litre), purchase protection, and basic travel insurance.

That said, because this is a personal credit card, using it for business purposes could affect your personal credit and make bookkeeping more complex.

Key benefits:

- 0% interest on balance transfers for 10 months (1% fee)

- Low post-promo APR of 13.99%

- Annual fee rebated for year one

- Fuel savings and insurance perks

- Not ideal for multi-user business environments

MBNA True Line Mastercard (Personal)

Best for: Individuals looking to eliminate high-interest debt with no annual fee.

The MBNA True Line Mastercard is a personal card that offers a 0% promotional interest rate on balance transfers for 12 months — the longest offer on this list. It’s one of the most popular consolidation tools for Canadians with existing card balances.

It comes with no annual fee, and once the promo ends, you’ll pay 12.99% on purchases and 17.99% on future balance transfers.

However, it’s not designed for business use. There are no business-specific perks, no expense tracking tools, and no integrations with accounting platforms. It’s best viewed as a short-term tool for individuals — not a long-term business solution.

Key benefits:

- 0% APR on balance transfers for 12 months

- $0 annual fee

- Low purchase APR (12.99%) after promo

- Limited features for business owners

- No cashback, spend controls, or accounting support

How to Choose a 0% Interest Business Card in Canada

When comparing 0% interest card options, it's tempting to focus solely on the promotional rate — but that’s only one part of the equation. Here’s what Canadian business owners and finance leads should consider before choosing a card:

1. Is the 0% interest offer temporary or permanent?

Promotional balance transfer rates (e.g., 0% for 10–12 months) are useful for debt consolidation, but costs can spike when the promo ends. In contrast, corporate cards like Venn offer ongoing 0% interest by design, with no future APR surprises.

2. Will this card impact your personal credit?

Many 0% APR options are personal cards used for business purposes. That may blur the line between personal and business finances, complicate tax filing, or impact your credit utilization ratio. A true corporate card keeps liability with the business.

3. Does the card support team access and spending controls?

Personal cards lack essential tools like virtual card issuing, per-employee limits, and real-time spend tracking — all standard on corporate platforms.

4. Can the card integrate with your accounting tools?

Look for platforms that support two-way sync with QuickBooks or Xero. This saves hours during reconciliation and reduces the risk of human error.

5. Are there FX fees or limits on rewards?

International vendors and USD expenses are common for Canadian SMBs. Choosing a card with multi-currency support and uncapped cashback can unlock significant long-term value.

Why Canadian SMBs Are Moving Away from Traditional Credit Cards

Canadian businesses are increasingly shifting away from personal and traditional business credit cards — and for good reason.

Modern finance teams want tools that streamline workflows, not create new ones. Here’s why the switch to corporate card platforms like Venn is accelerating:

- No personal risk – Venn doesn’t require personal guarantees or affect your credit score

- Real-time visibility – Instant updates on who’s spending what, where, and why

- Zero interest, always – Not a gimmick or promo, just smart spend logic

- Multi-currency agility – Spend in CAD, USD, GBP, or EUR without juggling card types

- Integrated everything – Payments, reconciliations, and approvals in one platform

Traditional cards were built for an era before cloud accounting, distributed teams, or global freelancers. Corporate cards are built for what business looks like today.

Summary: Which 0% Interest Card Is Right for Your Business?

If your business is looking to reduce interest costs, smooth out cash flow, or consolidate spending, there’s no shortage of “0% APR” options in Canada — but they’re not all created equal.

- Choose Venn if you want a truly interest-free solution with cashback, multi-currency support, and full control over spend and accounting. There’s no promotional window to worry about, and no personal liability involved.

- Go with BMO or CIBC if your priority is consolidating short-term debt and you’re comfortable using a personal or traditional credit product for your business.

- Opt for Amex Business Platinum if you want points and perks, travel often, and have the volume to justify the high annual fee.

- Consider MBNA only if you’re consolidating debt personally or bridging startup expenses — but know that it’s not built for long-term business needs.

Ultimately, the best option depends on your business structure, growth stage, and how you plan to use the card. But if you’re looking for 0% interest with none of the strings, Venn is the only one that offers it by design, not as a teaser.

Call to Action: Make Your Business Spending Work Harder

Stop overpaying in interest or relying on personal cards for business needs.

With the Venn Corporate Card, you get:

- 0% interest, always

- 1% cashback on every dollar spent

- Real-time visibility and spend controls

- Seamless integration with your accounting software

- Global payment capabilities, all in one card

Switch to smarter business spending — get started with Venn today

FAQ: 0% Interest Business Credit Cards in Canada

Q: What does 0% interest mean for business credit cards?

A traditional business credit card offering 0% interest (or 0% APR) provides a temporary promotional period, typically lasting from 9 to 20 months, where no interest is charged on new purchases or balance transfers. This is a financing tool. In sharp contrast, a corporate charge card does not charge interest at all, not as a limited-time offer, but as a permanent feature of its design.

Q: What’s the difference between a 0% APR and a charge card?

The core difference lies in the revolving credit mechanism. A 0% APR credit card is a revolving credit product that temporarily waives interest, but allows you to carry a balance (debt) that will eventually incur high interest. A charge card, like Venn's, is not revolving credit; it requires you to pay the balance in full at the end of each statement period. Because you cannot carry a balance, there is no Annual Percentage Rate (APR), and thus, no interest ever accrues.

Q: Are there any 0% interest business credit cards in Canada right now?

Yes, but they are rare and are usually promotional offers. Most 0% interest options available in Canada are either balance transfer offers on personal cards (often for 6 to 12 months) or short-term purchase offers on select business cards. If you want a spend solution that offers permanent 0% interest built into its structure, a corporate charge card platform like Venn is one of the only solutions available specifically for incorporated Canadian businesses.

Q: What happens when the 0% period ends?

With traditional 0% APR cards, once the promotional window expires, the full standard Annual Percentage Rate (APR) immediately applies to any unpaid balance. This standard rate is often high, typically ranging from 17.99% to over 25%. This can lead to a significant and sudden increase in costs if the debt hasn't been paid off. With a corporate charge card that has no APR, there is no risk of surprise interest charges at any point.

Q: Is it better to use a personal or business credit card for my company?

It is far better to use a dedicated business or corporate card. While using a personal card might seem easier initially, it complicates tax preparation, blurs the legal distinction between you and your company (risking personal liability), and does not help you build credit in your business's name. Business-specific or corporate cards are designed for multi-user spend control and keep liability and reporting separate from your personal finances.

This publication is provided for general information purposes and does not constitute legal, tax or other professional advice from Venn Software Inc or its subsidiaries and its affiliates, and it is not intended as a substitute for obtaining advice from a financial advisor or any other professional. We make no representations, warranties or guarantees, whether expressed or implied, that the content in the publication is accurate, complete or up to date.

Venn is all-in-one business banking built for Canada

From free local CAD/USD accounts and team cards to the cheapest FX and global payments—Venn gives Canadian businesses everything they need to move money smarter. Join 15,000+ businesses today.

Frequently asked questions

Everything you need to know about the product and billing.

Join 15,000+ businesses banking with Venn today

Streamline your business banking and save on your spend and transfers today

No personal credit check or guarantee.